If you’re not a U.S. resident and want tax treaty benefits from the U.S., IRS Form 8833 is what you need. This form helps you save money and makes your U.S. tax duties easier. Filing late or incorrectly may result in penalties of up to $1,000 for individuals or $10,000 for corporations. But, no need to panic!

Our SAL Accounting guide explains what Form 8833 is and gives you clear instructions. We also share tips to avoid penalties. Follow our guide, and we’ll show you how to save cash.

Quick Takeaways

- Form 8833 helps non-U.S. residents claim tax treaty benefits to lower U.S. taxes.

- File Form 8833 with your tax return by April 15 to avoid $1,000/$10,000 penalties.

- Pension recipients and FDAP filers with Form 1042-S don’t need to file Form 8833.

- List income, treaty article, and payor details on Form 8833 to claim benefits.

- Avoid errors like missing IDs or vague claims to prevent IRS rejection.

What is IRS Form 8833?

IRS Form 8833, “Treaty-Based Return Position Disclosure,” lets non-U.S. residents, expats, and businesses use tax treaties to lower U.S. taxes on dividends or royalties (Source). For example, a Canadian can cut dividend taxes from 30% to 15%. Filing it stops double taxation, avoids IRS fines, and keeps you in the clear. Get it right with our cross-border tax accountant to make it easy.

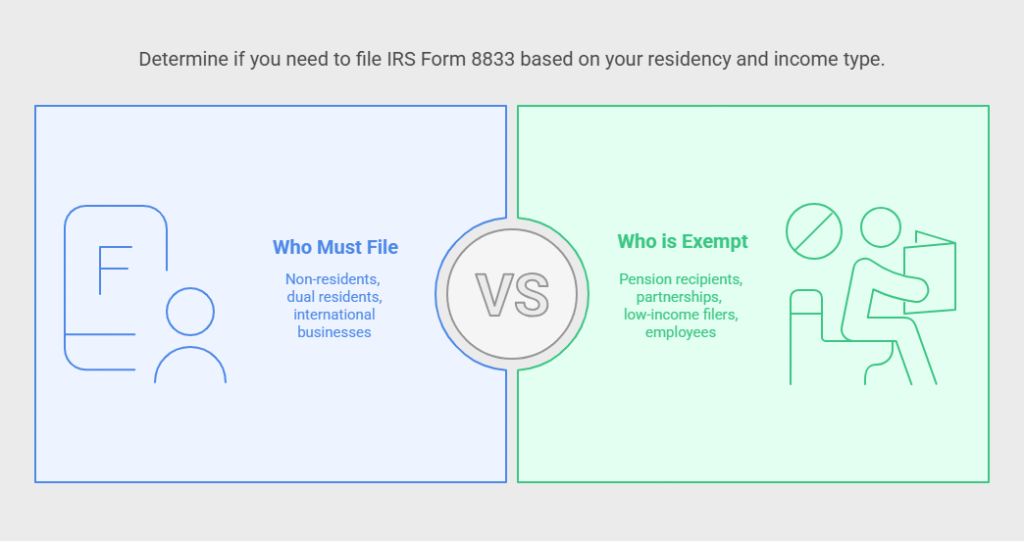

Who Needs to File Form 8833?

Not everyone claiming the U.S.-Canada tax treaty needs IRS Form 8833, but some taxpayers, like those opening a U.S. LLC as non-residents, must file to stay compliant. It’s for those whose treaty benefits change U.S. tax rules, saving them from double taxes in the U.S. and countries like Canada. Here’s who needs to file the form:

- Non-U.S. Residents: Non-residents receiving U.S. dividends file Form 8833 to claim a lower tax rate, like 15% instead of 30%.

- Dual Residents: People living in both the U.S. and another country file Form 8833 to set their residency and avoid certain U.S. taxes.

- International Businesses: Companies from other countries file Form 8833 to avoid taxes on U.S. property gains under a tax treaty.

Pro Tip: Check Article 4 of the U.S.-Canada treaty if you live in both countries. It helps you pick your tax residency for Form 8833.

Who is Exempt from Filing Form 8833?

Some people can skip filing Form 8833 based on IRS rules. Here’s who doesn’t need to deal with the extra paperwork:

Pension or Social Security Recipients

Residents of countries with U.S. tax treaties, like Canada, getting U.S. Social Security or pensions don’t need it. The treaty covers them automatically. No extra filing needed.

Partnership or Trust Filers

Non-residents in a U.S. partnership or trust don’t need Form 8833. The partnership or trust takes care of your treaty benefits. You’re set without extra filing.

Low-Income FDAP Filers

If your dividends or similar income are reported on Form 1042-S with the correct treaty withholding, you don’t need Form 8833. The IRS accepts that form instead.

Dependent Personal Services

Employees earning wages, like a Mexican consultant at a U.S. company, don’t need Form 8833. Payroll handles your treaty benefits. You’re good without extra filing.

Pro Tip: Save your Social Security records. They prove treaty benefits if the IRS questions your Form 8833 exemption.

Check out this table to quickly see who’s exempt from filing Form 8833:

| Exempt Group | Criteria | Example |

| Pension/Social Security Recipients | Treaty automatically applies (e.g., Article 18) | Canadian retiree with U.S. Social Security |

| Partnership/Trust Filers | Entity handles treaty benefits (e.g., Form 1065, 1041) | Canadian in a U.S. trust |

| Low-Income FDAP Filers | Income reported on Form 1042-S with correct treaty withholding | Canadian with $5,000 U.S. dividends |

| Dependent Personal Services | Payroll applies treaty benefits (e.g., Article 15) | Canadian consultant for U.S. firm |

IRS Form 8833 Filing Guide: When and How to File

This IRS Form 8833 filing guide shows you how to file the form right to secure tax treaty benefits and avoid penalties. Filing correctly keeps you on the IRS’s good side and saves your cash. Below are easy points for when and how to file it:

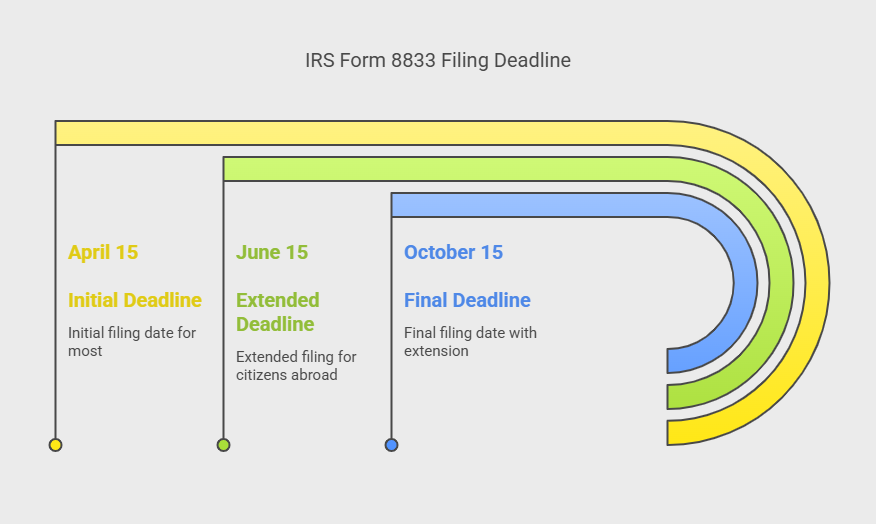

Filing Deadlines

Form 8833 goes with your U.S. tax return by the due date, or you risk big fines. Your deadline depends on who you are and where you live. You can get extra time if needed.

- April 15: Most people, like non-residents filing Form 1040-NR or businesses filing Form 1120-F, file by this date.

- June 15: U.S. citizens or residents living abroad get until this date.

- October 15: Ask for an extension with Form 4868, and you’ve got until this date.

Filing Methods

You usually send Form 8833 with your U.S. tax return to claim withholding taxes under the U.S.-Canada tax treaty. But there are other ways if you don’t need a return or want to e-file. Picking the right method keeps you safe from penalties. Here’s how you can submit the form:

- With Tax Return: Attach Form 8833 to Form 1040-NR for non-residents or 1120-F for businesses when you file.

- Separate Filing: Without a return, send Form 8833 to the IRS Service Center, like Austin, with your name and ID number (SSN, ITIN, or EIN).

- E-Filing: Use tax software that handles Form 8833, but double-check it works to send it correctly.

Compliance Essentials

Filing Form 8833 correctly matters a lot to avoid fines and stay cool with the IRS when claiming treaty benefits. A few simple steps help you avoid mistakes and audit trouble. Here’s what to do to nail it:

- Check Treaty Details: Look at IRS Tax Treaty Tables (here) to make sure you’ve got the right treaty article and benefits.

- Save Records: Keep income papers, like Form 1042-S, in case the IRS audits you.

- Fix Late Filings: Explain a good reason for late filing, like sudden delays, to request an IRS penalty waiver.

Pro Tip: Keep your tax return handy. It supports Form 8833 if the IRS checks cross-border filings.

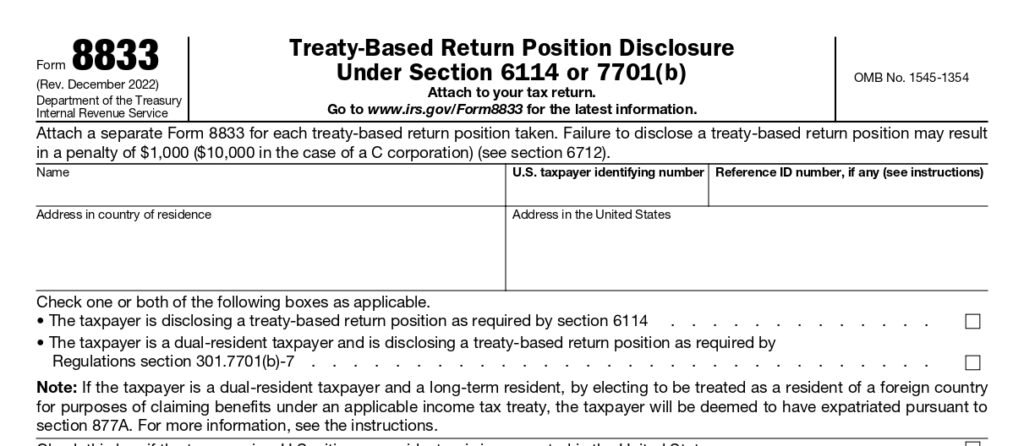

Form 8833 Instructions: How to Complete the Form Step-by-Step + Example

We’ll guide you through filling out Form 8833 to claim tax treaty benefits. An example makes it super clear:

1.Fill Out the Header Info

Start Form 8833 with your details. Add your full name and SSN/ITIN (individuals) or EIN (businesses). List your home country address. Include a U.S. address if you’re a dual resident. Check section 6114 (treaty claim) or dual-resident status. Skip the U.S. citizen box unless it applies. Match your tax return to avoid IRS trouble.

Pro Tip: Use the same name and ID as your tax return. It avoids IRS mix-ups.

Example: Emma Chen, a Canadian, runs a U.S. consulting LLC making $50,000 in 2024. She claims a U.S. tax exemption under U.S.-Canada Treaty Article 7, with no U.S. permanent establishment. She files Form 8833 with Form 1040-NR to skip the 30% tax (Section 871(a)). Here’s what she puts in the form’s header:

- Name: Emma Chen

- ITIN: 123-45-6789

- Address: 456 Oak St., Vancouver, BC V6B 2M1, Canada

- U.S. Address: (Blank because she lives and operates in Canada, with no U.S. address.)

- Check: Section 6114

- U.S. Citizen: (Unchecked)

We’ll use Emma’s details to guide you through filling out the rest of Form 8833. Each step includes her info as an example.

2.Add Your Info (Line 1)

Name the treaty country you’re using. Write the full country name, not abbreviations. List the specific treaty article and paragraph you rely on. Use IRS Tax Treaty Tables to find the right article. This shows the IRS your treaty claim.

Example: Emma names “Canada” and lists “Article 7, Paragraph 1” for business profits exempt from U.S. tax.

3.List Your Treaty Country (Line 2)

Name the country with the tax treaty you’re using, like Canada. Add your address in that country, same as Line 1 if you live there. Write the full name of the country, like “Canada,” not “CA.” This shows you’re a resident who qualifies for treaty benefits.

Example: Emma cites “Section 871(a)” for non-resident tax on business income, overruled by the treaty.

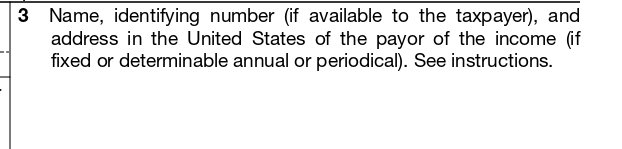

4.Describe Your Income (Line 3)

Tell the IRS what income you’re claiming benefits for, like dividends and royalties, or avoid US LLC double taxation for Canadians. Include the U.S. tax code section it connects to, like Section 871(a) for non-residents. For example, note if you’re claiming $10,000 in dividends. This helps the IRS follow your claim.

Pro Tip: Review your income records before listing amounts on Line 3. It confirms you claim the right benefits.

Example: Emma states “$50,000 consulting income, Section 871(a), from U.S. Client Co., EIN 12-3456789, 789 Pine St., Seattle, WA 98101.”

5.Choose the Treaty Article (Line 4)

Pick the specific treaty article and paragraph, like Article 10, Paragraph 2 of the U.S.-Canada treaty for dividends. Say if you meet any Limitations on the Benefits test, like living in Canada. Look up the treaty on IRS Tax Treaty Tables to avoid mistakes that could ruin your claim.

Pro Tip: Read your treaty’s summary online to pick the right article for Line 4. It keeps your claim solid.

Example: Emma writes “Article XXIX-A, Paragraph 2” as a Canadian resident meeting the LOB test.

6.Show the Tax Code Change (Line 5)

Note that in the U.S. tax code section, the treaty changes, like Section 881 for foreign businesses. It’s often the same as Line 3 but highlights the rule the treaty overrides. Be clear to prevent mix-ups with the IRS.

Example: Emma checks “No” for her standard business income claim.

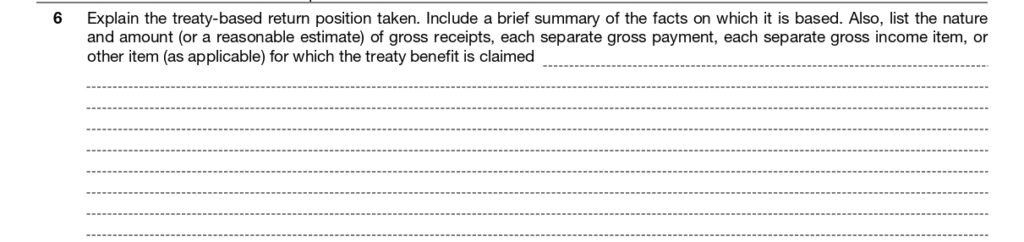

7.Explain Your Claim (Line 6)

Describe your treaty claim fully. List the income amount, facts that back your claim, and how the treaty cuts your taxes. Good details stop the IRS from asking questions later.

Example: Emma writes, “Emma Chen, Canadian at 456 Oak St., Vancouver, BC V6B 2M1, earned $50,000 from U.S. Client Co. Article 7, Paragraph 1 exempts U.S. tax (Section 871(a)), no U.S. permanent establishment, saves $15,000.”

- Read More: “Reporting Foreign Business Income in Canada“

Check out the full Form 8833 image below to guide your filing:

Common Mistakes When Filing Form 8833 and How to Avoid Them

Filing Form 8833 wrong can mess up your non-resident tax exemption in the U.S. and cost you big penalties. Here, we will share common mistakes and easy fixes to keep your filing smooth:

- Missing Taxpayer ID: Forgetting your SSN, ITIN, or EIN confuses the IRS. It slows your claim or brings penalties.

Fix: Check your ID number on tax documents and add it to the form.

- Wrong Treaty Article: Selecting the wrong article, such as an incorrect U.S.-Canada treaty section, eliminates your tax benefits.

Fix: Look up the right article and paragraph on IRS Tax Treaty Tables for Line 4.

- Not Attaching Form: Skipping Form 8833 with your tax return, like Form 1040-NR, causes trouble. Not mailing it separately without a return adds issues.

Fix: Attach Form 8833 to your return or mail it to the IRS Service Center, like Austin, for Form 1040-NR.

- Vague Line 6 Explanation: A weak Line 6, like missing income details or treaty benefits, puzzles the IRS and risks rejection.

Fix: Write a clear Line 6 with income amount, facts, and how the treaty lowers taxes.

Case Study: Fixing a Canadian’s Form 8833 Errors

Problem: A Canadian consultant called us. They missed their ITIN on Form 8833. Their vague Line 6 explanation for $35,000 in 2024 income delayed their claim.

What I Did: I advised resubmitting with the correct ITIN, matching Form 1040-NR. I suggested using a U.S.-Canada treaty sample to detail Line 6 with income and treaty facts.

The Result: The IRS processed the revised form quickly. The consultant avoided a $1,000 fine and secured treaty benefits, saving thousands.

- Read More: “How to Open an LLC in the US From Canada“

Take a look at this table to avoid common filing mistakes:

| Common Mistake | Consequence | Fix |

| Missing Taxpayer ID | Delays claim, risks penalties | Check SSN/ITIN/EIN on tax documents for Line 1 |

| Wrong Treaty Article | Loses tax benefits | Use IRS Tax Treaty Tables for Line 4 |

| Not Attaching Form | IRS rejects claim | Attach to Form 1040-NR or mail to Austin |

| Vague Line 6 Explanation | Risks IRS rejection | Detail income, facts, treaty benefits in Line 6 |

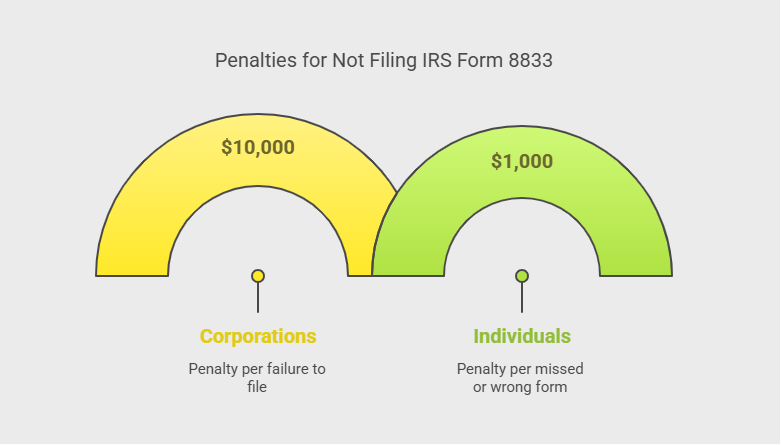

Penalties for Not Filing IRS Form 8833

Skipping Form 8833 or getting it wrong can lead to financial penalties. This form is key for claiming tax treaty benefits, and The IRS takes it seriously. Here’s the rundown on penalties and how to avoid them. If you don’t file Form 8833 for a treaty-based position, you’ll owe:

- Individuals: $1,000 per missed or wrong form. Each treaty position you skip counts as a separate fine.

- Corporations: $10,000 per failure, with the same rules applying.

- Additional Penalties

Slip-ups with Form 8833 can snowball into bigger problems, like:

- Late Filing: Corporations filing past the deadline (or extended deadline) without a good reason face a $10,000 fine.

- Negligence or Disregard: Ignoring tax rules adds a 20% penalty on any taxes you underpay.

- Substantial Understatement: Underreporting taxes significantly adds a 20% penalty to your tax bill.

- Denied Treaty Benefits: Skip or botch Form 8833, and the IRS might block your treaty benefits.

- Relief Options

You might sidestep penalties with these options:

- Reasonable Cause: A solid excuse like a family emergency or natural disaster helps. Submit proof to secure an IRS penalty waiver. They set strict standards for valid reasons.

- First-Time Abate: If you’ve been penalty-free for three years and filed all returns, you could get a one-time pass. Call the IRS, file Form 843, or send a statement with evidence.

Case Study: Escaping a Penalty for a Mississauga Business Owner

Problem: A Mississauga business owner got in touch with us after skipping Form 8833 for U.S. royalties. The IRS issued a $10,000 fine for missing the treaty disclosure, risking their tax breaks.

What I Did: I helped file Form 843, submitting proof of a medical emergency that halted their filing to request a reasonable cause waiver and erase the penalty.

The Result: The IRS removed the $10,000 fine. The owner kept their treaty benefits, saving thousands with no tax headaches.

Book a consultation with our cross-border accountants to ensure accurate Form 8833 filing.

Final Thoughts

Form 8833 is easy to handle with clear details. Our guide simplifies IRS Form 8833 for non-U.S. residents claiming U.S. tax treaty benefits. Clear steps, handy examples, and tips help you avoid mistakes, skip double taxes, and escape penalties. You’ll file right and save money easily.

Need more help with Form 8833? Reach out to our team at SAL Accounting for expert support. Contact us for a smooth filing process.

Frequently Asked Questions (FAQs)

Form 8833 lets non-U.S. residents claim tax treaty benefits to cut U.S. taxes, avoid double taxation, and dodge $1,000/$10,000 penalties.

Complete Form 8833 with your details, treaty, and income. Attach it to your tax return or mail it to the IRS Service Center.

You risk a $1,000 (individual) or $10,000 (corporation) penalty per position, plus double taxation or extra fines.

Yes, e-file Form 8833 with your return using supported tax software. Verify it is submitted correctly.

No, exemptions include pension recipients, partnership/trust filers, FDAP filers with Form 1042-S, and payroll-handled employees.

Dual residents check the dual-resident box, claim foreign residency, and attach Form 8833 to Form 1040-NR with residency proof.

Keep Form 1042-S, contracts, payor details, and residency proof to back your claim for audits.

Yes, mail Form 8833 separately to the IRS Service Center with your name and ID if no return is filed.