Thinking about setting up a U.S. LLC under your Canadian corporation? It can look like a simple way to expand into the U.S., especially if you’re selling to American customers, opening a U.S. bank account, or using U.S. suppliers or warehouses.

But the setup is only one part of the decision. The bigger issue is how the U.S. and Canada will treat the LLC for tax purposes. At SAL Accounting, we help Canadian businesses make sense of cross-border structures like U.S. LLCs. In this guide, we’ll walk through how ownership works, where double taxation can happen, what filings may apply, and what to check.

For Shopify sellers, the LLC question is simple: do the numbers make sense? This U.S. LLC cost calculator for Shopify sellers helps compare the possible savings with the extra cross-border costs.

Quick Takeaways

- A Canadian corporation can own a U.S. LLC.

- You do not need to be a U.S. citizen or resident to form a U.S. LLC.

- The main challenge is usually tax treatment, not the formation process.

- The IRS and CRA may treat the same LLC differently.

- That mismatch can create double taxation if the structure is not planned properly.

- A foreign-owned U.S. disregarded entity may need to file Form 5472 with a pro forma Form 1120 when the rules apply.

- Canadian corporations may also have CRA reporting obligations, including Form T1134 where foreign affiliate rules apply.

- In some cases, a U.S. corporation, limited partnership, or another structure may be cleaner than a U.S. LLC.

Can a Canadian Corporation Own a U.S. LLC?

Yes. A Canadian corporation can own a U.S. LLC. The setup is usually manageable. You choose a state, appoint a registered agent, file the LLC documents, and apply for an EIN. These steps are similar to opening an LLC in the U.S. from Canada.

But the tax side needs more attention. The U.S. may treat the LLC differently depending on its LLC tax classification, while Canada may see it differently. That mismatch is where cross-border problems usually begin.

For Canadian owners who want the entity formed with the cross-border tax pieces in mind, SAL can help set up a U.S. LLC as a non-resident.

Why Canadian Businesses Consider the U.S. LLC

Canadian businesses usually consider a U.S. LLC when their U.S. activity starts growing. That could mean more U.S. customers, a U.S. bank account, a U.S. warehouse, or contracts with American vendors.For e-commerce businesses, this can happen quickly.

Example: your Canadian Shopify store starts selling more in the U.S. You open a U.S. bank account, use a U.S. warehouse, and receive payouts from Shopify, Amazon, Stripe, or PayPal.

Now the LLC may look useful, but the real question is whether it makes your tax, banking, and bookkeeping cleaner, or just adds more work. That is why selling internationally on Shopify often needs to be looked at alongside the business structure.

The Main Tax Issue: Canada and the U.S. May See the LLC Differently

This is the part that matters most. In the U.S., a single-member LLC is often treated as a disregarded entity by default. That means the income may flow up to the owner instead of being taxed inside the LLC. But Canada may not see it the same way. The CRA can treat the U.S. LLC as a separate entity. So the same income may be viewed differently in each country. That mismatch can create:

- U.S. tax reporting

- Canadian tax reporting

- Foreign tax credit questions

- Related-party reporting

- Possible double taxation

Example: your Canadian corporation may own a U.S. LLC that earns profit from U.S. sales. The IRS may see the income as flowing to the Canadian corporation, while Canada may treat the LLC as a separate foreign entity.

That is why this topic often connects to double taxation between Canada and the U.S.. The point is, the LLC itself is not always the problem. The problem is choosing the structure before checking how both countries will treat it.

| Issue | U.S. view | Canadian view | Why it matters |

| Single-member LLC | Often disregarded | Often separate entity | Tax mismatch |

| Income reporting | May flow to owner | May stay with LLC | Double-tax risk |

| Related transactions | May trigger Form 5472 | May need support | Filing exposure |

| Treaty position | May help | Not automatic | Needs planning |

The point is, the LLC itself is not always the problem. The problem is choosing the structure before checking how both countries will treat it. That is how many owners end up with U.S. LLC tax problems for Canadians, even when the LLC itself was easy to open.

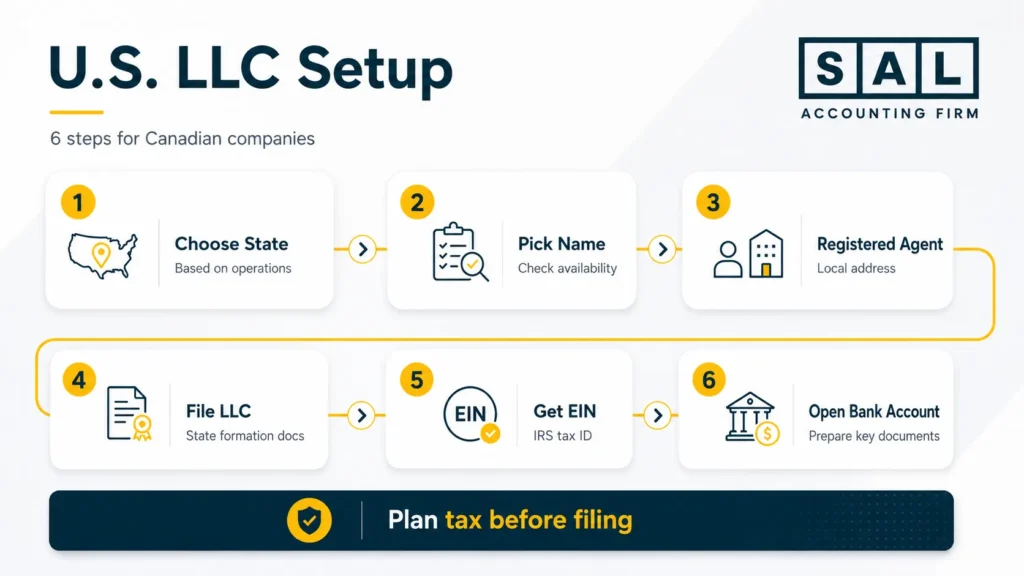

How to Set Up a U.S. LLC as a Canadian Corporation

Setting up the LLC is usually the easier part. The planning should happen before or during the setup, not months later when the first tax filings are due.

Step 1: Choose the Right State

Your LLC must be formed in a U.S. state. Delaware, Wyoming, and Nevada are popular, but they are not always the best fit. If your business stores inventory, hires people, or creates tax obligations in another state, you may still need to register there too. This can matter if you are opening a business in Florida as a Canadian.

Choose the state based on how your business actually operates, not just because a state is popular online.

| State | Income Tax | Legal Protection | Annual Fees | Best For | Notes |

| Delaware | No income tax on LLCs | Strong, established | $90 (approx.) | Large and international firms | Additional taxes if operating outside Delaware |

| Wyoming | No income tax | Minimal regulations | $50 – $100 | Privacy-focused businesses | Limited legal tools for big businesses |

| Nevada | No income tax | Strong business laws | $200 (approx.) | Privacy and tax savings | Higher annual fees than other states |

- Pro Tip: Delaware is popular for big corporations, but Wyoming could be a better fit for smaller businesses or Canadian companies. It’s cheaper, tax-friendly, and easier to manage.

Step 2: Pick a Name for the LLC

Your LLC name must follow state rules and usually needs to include “LLC” or “Limited Liability Company.” You should also check whether the name is available and whether it creates trademark or branding issues.

Example: your legal LLC name, Shopify store name, and Amazon seller name may not all be the same. That is why the naming step often sits beside the wider tax setup for a Shopify seller.

Step 3: Appoint a Registered Agent

Every U.S. LLC needs a registered agent in the state where it is formed. This person or service receives legal notices, state mail, and official documents for the LLC.

If your Canadian corporation does not have a physical address in that state, you can usually hire a registered agent service. It is one of the practical steps involved when you register a business in the U.S. from Canada.

Step 4: File the LLC Formation Documents

To create the LLC, you file formation documents with the state. These are often called Articles of Organization or a Certificate of Formation.

The filing usually includes your LLC name, registered agent, business address, ownership details, and filing fee. Keep copies of everything. You may need them for your EIN, bank account, payment processors, and tax filings.

Step 5: Get an EIN from the IRS

Your LLC will usually need an Employer Identification Number, or EIN. You may need an EIN to open a U.S. bank account, file U.S. tax forms, work with platforms, or hire employees, and the application is tied to Form SS-4.

For Canadian owners, this step can feel confusing because the responsible party may not have a U.S. SSN. That is why EINs for Canadian companies often become part of the setup conversation. The main thing is to get the EIN early, so banking and platform setup do not get delayed.

Step 6: Open a U.S. Bank Account

A U.S. bank account can help separate U.S. sales, expenses, vendor payments, and platform payouts. For e-commerce businesses, this matters because platform sales and bank deposits rarely match.

Example: Shopify shows $50,000 in U.S. sales, but only $43,500 lands in the bank. That difference may include fees, refunds, discounts, chargebacks, currency conversion, shipping adjustments, or sales tax. Most banks may ask for:

- EIN letter from the IRS

- LLC formation papers

- Proof of your Canadian corporation

- Photo ID, such as a passport

- U.S. address, if required

This step often overlaps with opening a U.S. bank account from Canada. A bank account helps keep activity cleaner, but it does not fix the books by itself. You still need sales, fees, refunds, tax, and transfers recorded properly.

➜ Read more: Can a Canadian Own a Business in the US?

U.S. Tax and Filing Requirements for a Canadian-Owned LLC

A Canadian-owned U.S. LLC may have U.S. tax and information filing requirements. The exact forms depend on how the LLC is classified, whether it has one owner or multiple owners, whether it earns U.S.-source income, whether it has U.S. trade or business activity, and whether it has transactions with related parties. Common U.S. forms may include:

- Form SS-4 for the EIN

- Form 5472 for certain foreign-owned U.S. entities with reportable transactions

- Pro forma Form 1120 when required for a foreign-owned disregarded entity

- Form 8832 if the LLC elects a different tax classification

- Form 1065 if the LLC is taxed as a partnership

- Form 1120 if the LLC elects to be taxed as a corporation

- Treaty disclosure forms where treaty positions are taken

Form 5472 is especially important. The IRS uses Form 5472 to report certain transactions between a reporting corporation and a foreign or domestic related party. The IRS instructions also state that a foreign-owned U.S. disregarded entity may need to file a pro forma Form 1120 with Form 5472 attached.

For many Canadian-owned LLCs, Form 5472 filing requirements are one of the first U.S. filing issues to review.

In some cases, U.S. filing questions may also overlap with foreign corporation reporting, including Form 1120-F. This is not meant to scare you. It just means the filing calendar matters. Once the structure is mapped clearly, these forms are much easier to manage.

Tax Reporting Requirements for the U.S. LLC Owned by a Canadian Corporation

Owning a U.S. LLC through a Canadian corporation can also create Canadian reporting. Depending on the structure, the corporation may need to report foreign affiliate information, income from the U.S. entity, foreign taxes paid, and related-party transactions. Common Canadian reporting may include:

- T2 corporate income tax return

- T1134, where foreign affiliate reporting applies

- T5013, where partnership reporting applies

- Foreign tax credit support

- Transfer pricing records for related-party transactions

- Form T1135 foreign asset reporting, where applicable

This is where many owners get stuck. They open the LLC, start operating, and only later realize Canada may treat the structure differently than expected.

The better move is to map the reporting before money starts moving. The goal is not just to open the entity. It is to understand what the structure will do to your taxes, filings, banking, and books.

Double Taxation Risk for Canadian Corporations Owning a U.S. LLC

Double taxation can happen when the same income is caught by both U.S. and Canadian tax rules, and the credits or treaty relief do not line up cleanly.

For example, your Canadian corporation may own a U.S. LLC that earns U.S. income. The U.S. may tax that income one way, while Canada may expect it to be reported another way. Foreign tax credits may help, but they do not always fix the full issue. The Canada-U.S. tax treaty may also help in some cases, but treaty relief is not automatic.

Pro Tip: Double taxation planning is not about finding one magic form. It is about making sure the full structure works from both sides.

Case Study: Avoiding Double Taxation for a Toronto Tech Business1

The Problem: A Toronto tech company (downtown near the CN Tower) faces heavy double taxation: 21% US federal corporate tax on income, plus 26.5% combined federal + Ontario tax in Canada. Nearly half the profits disappear.

What We Do: We avoid the usual Form 8832 election. Instead we use these approaches:

- No US physical presence: We apply the Canada-US Tax Treaty (Article V) and file IRS Form 8833. This shows no US permanent establishment exists, so profits are taxed only in Canada—no US tax, no double taxation.

- With some US operations: We set up arm’s-length management fees from the US LLC to the Toronto parent for services (strategy, admin, etc.). We keep fees reasonable and documented to shift profits north and reduce the overall tax hit.

The Result: Effective tax drops to roughly the Canadian rate (26.5% for Ontario corporations). The business keeps far more profit to reinvest in Toronto growth or US expansion—without the double-tax pain.at 21% US tax hit. Our client got a great setup that works with both tax rules, and they could focus more on running their business.

Common Problems With Canadian-Owned U.S. LLCs

A U.S. LLC can work well in the right situation. But when the setup is rushed, these issues usually show up.

| Problem | What happens | Why it matters | Better move |

| No tax review | LLC opened too fast | Wrong setup | Review first |

| Messy payouts | Sales ≠ deposits | Bad reporting | Reconcile payouts |

| Related-party gaps | Money moves between entities | Filing risk | Track transfers |

| Sales tax confusion | Sales tax mixed with income tax | State risk | Check nexus |

| No filing calendar | Deadlines missed | Penalties | Map deadlines |

1. The LLC Is Opened Before the Tax Structure Is Reviewed

This is one of the most common issues. The owner forms the LLC because it seems quick and affordable. Then the tax questions come later.

By the time income starts flowing, the company may already have U.S. filings, Canadian reporting, related-party transactions, bank activity, platform payouts, sales tax exposure, or a tax classification that does not fit. That is why Canada vs. U.S. incorporation tax considerations should be reviewed before the structure is active.

The fix: review the tax structure before forming the LLC or before the LLC starts operating.

2. Platform Sales Do Not Match Bank Deposits

For e-commerce businesses, this is a big one.

Example: Shopify shows $100,000 in U.S. sales, but only $87,000 lands in the bank. That does not mean your revenue is $87,000. The difference may include payment fees, refunds, discounts, chargebacks, sales tax, app fees, shipping, marketplace fees, or currency conversion.

If the U.S. LLC is added to the structure, the accounting needs to show what actually happened. This connects closely to e-commerce payment reconciliation, because the issue is not just the sale. It is what happened between the platform and the bank.

The fix: track sales, payouts, fees, refunds, inventory, and bank deposits from the beginning.

3. Related-Party Transactions Are Not Tracked

If your Canadian corporation owns the U.S. LLC, money may move between related parties. For example, the Canadian corporation may pay U.S. expenses, the U.S. LLC may send money back to Canada, or one entity may reimburse the other.

These transactions need clean records. They may affect Form 5472, transfer pricing, treaty positions, and Canadian reporting. This is where Canada-U.S. transfer pricing can become relevant.

The fix: keep clear records of every transaction between the Canadian parent and the U.S. LLC.

4. Sales Tax Is Treated Like Income Tax

U.S. sales tax is separate from income tax. If your LLC sells to U.S. customers, stores inventory in the U.S., or sells into multiple states, sales tax rules may apply.

For Canadian sellers, this often connects to U.S. sales tax requirements for Canadian sellers andsales tax nexus for sellers.

The fix: check sales tax nexus by state, sales channel, and inventory location.

5. The Filing Calendar Is Not Clear

Cross-border structures often involve several forms and deadlines. The problem is not always the tax itself. Sometimes the issue is simply that no one knows what needs to be filed or when.

A financial calendar with key deadlines can help keep Canadian filings, U.S. forms, sales tax deadlines, and platform reporting from turning into a year-end scramble.

The fix: create a filing calendar for both countries before year-end.

Alternative U.S. Business Structures for Canadian Corporations

| Structure | Best fit | Main benefit | Watch for |

| U.S. LLC | Flexible U.S. activity | Simple setup | Tax mismatch |

| U.S. C-Corp | Larger U.S. operations | Clearer entity | Double tax layer |

| Limited partnership | Specific planning | Flexible ownership | More filings |

| U.S. subsidiary | Growing U.S. presence | Cleaner split | Transfer pricing |

Option 1: Canadian Corporation Owns a U.S. LLC

This is the structure most people ask about first. It may work when the business wants a U.S. entity, U.S. banking, and operational flexibility.

Pros:

- Flexible U.S. structure

- Supports U.S. banking and contracts

- Common in the U.S.

- Useful for some operating businesses

Cons:

- Canada and the U.S. may treat it differently

- Double taxation risk

- Form 5472 may apply

- Canadian reporting may apply

- Related-party records need to be clean

The LLC may be useful, but it should not be the default answer.

Option 2: Canadian Corporation Owns a U.S. C-Corporation

A U.S. corporation can be cleaner in some cases because both countries generally recognize it as a corporation. That can make the tax structure easier to understand than an LLC. But it can also create U.S. corporate tax and possible withholding tax when profits are paid back to Canada.

Pros:

- Clearer corporate structure

- Familiar U.S. subsidiary setup

- Useful for larger U.S. operations

- Easier to explain to banks or vendors

Cons:

- U.S. corporate tax may apply

- Dividend withholding may apply

- Canadian reporting still matters

- Intercompany agreements may be needed

- State filings may still apply

This structure connects closely to U.S. subsidiary taxes for Canadian companies, especially when U.S. activity is growing beyond a light presence.

Option 3: Limited Partnership Structure

A limited partnership may work in some cross-border planning situations, but it is usually more complex. It depends heavily on the business type, ownership, and risk profile.

For example, real estate investors may use partnership structures differently from e-commerce operators. That is why this option can sit close to the tax implications for Canadians owning U.S. property.

Pros:

- Useful in specific planning situations

- Can support some ownership structures

- Flexible in the right setup

- May fit real estate or investment cases

Cons:

- More filings

- Partner reporting

- More admin

- More complicated bookkeeping

- Usually not the simplest option for e-commerce sellers

This is not usually the “simple” option. It needs a clear reason.

Option 4: Separate U.S. Entity for U.S. Operations

Some Canadian businesses separate Canadian and U.S. activity more clearly. For example, the Canadian corporation may handle Canadian activity, while a U.S. entity handles U.S. operations. This can make sense when there are U.S. employees, U.S. inventory, U.S. contracts, or a growing U.S. customer base.

Pros:

- Cleaner reporting by country

- Better separation of activity

- Useful for growing U.S. operations

- Supports U.S. contracts and banking

Cons:

- Transfer pricing may apply

- Management fees need support

- Intercompany agreements may be needed

- State tax and sales tax still matter

- More admin than one simple company

For some businesses, this may look more like registering a subsidiary company as a foreigner than simply opening an LLC. The setup can help, but the books need to show what each entity is actually doing.

How to Choose the Best U.S. Business Structure for a Canadian Company

There is no one-size-fits-all answer. A Canadian corporation owning a U.S. LLC may be fine in one case and messy in another. Before choosing, look at:

- What the business sells

- Where the money comes from

- Where inventory sits

- How profits move back to Canada

- Which filings apply

- How much admin you can manage

For e-commerce, the structure needs to reflect how sales actually happen. That means Shopify sales, Amazon sales, marketplace payouts, payment processors, inventory, refunds, sales tax, and currency conversion.

For online stores, the best business structure for online retail depends on more than the entity name. It depends on how the business sells and gets paid.

Pro Tip: Do not choose the most complicated structure. The point is to choose the one you can actually manage and trust.

Final Thoughts: Should a Canadian Corporation Own a U.S. LLC?

Yes, a Canadian corporation can own a U.S. LLC. But the better question is whether the structure will actually make your U.S. expansion cleaner. For e-commerce businesses, that means understanding how sales, payouts, fees, refunds, tax filings, and money moving between Canada and the U.S. will be handled. A U.S. LLC can work, but it is not always the best fit.

The goal is to choose a structure you can understand, manage, and trust. If you want to review your options, you can get clear guidance from SAL Accounting.

FAQs About Canadian Corporations Owning a U.S. LLC

Yes. A Canadian corporation can own a U.S. LLC. The bigger issue is how the LLC will be taxed and reported in both Canada and the U.S.

Not usually. But the LLC needs a registered agent with a physical address in the state where it is formed. Some banks may also ask for a U.S. address, which is why best U.S. banks for Canadians can come into the setup decision.

Canada may treat a U.S. LLC differently than the U.S. does. That difference can create double taxation or extra reporting if the structure is not planned properly.

It depends on how the LLC is classified. Common forms may include Form 5472, pro forma Form 1120, Form 1065, Form 1120, Form 8832, or treaty disclosure forms. For many foreign-owned LLCs, Form 5472 is one of the first forms to review because related-party transactions can trigger reporting.

A Canadian corporation may need to report foreign affiliate information using Form T1134 where the rules apply. Other Canadian corporate reporting may also apply depending on income, ownership, and related-party transactions.

Yes. A Canadian corporation can apply for an EIN using IRS Form SS-4. The process may be different if the responsible party does not have a U.S. SSN or ITIN.

It depends on the business model, ownership, income, and long-term plan. An LLC may be flexible, but a C-Corporation may be cleaner in some cases. For larger U.S. operations, U.S. subsidiary taxes for Canadian companies may be more relevant.

Not by itself. Sales tax depends on where you sell, where inventory is stored, and whether you have nexus. If your U.S. sales are growing, the US economic nexus threshold calculator can help you check whether sales tax obligations may be coming up.

Sometimes. A U.S. LLC can help with U.S. banking, contracts, and operations, but it must be planned around sales channels, inventory, payouts, refunds, fees, and sales tax.

Not always. Many Canadian Shopify sellers can sell to U.S. customers without opening a U.S. LLC. The question becomes more important when U.S. sales, banking needs, inventory, or platform costs change.

Yes, but the bank will usually ask for the EIN, LLC formation documents, proof of the Canadian corporation, owner ID, and sometimes a U.S. address. The bank account helps separate U.S. activity, but the bookkeeping still needs to be set up properly.

Check how the LLC will be taxed in both countries, what forms apply, whether sales tax is involved, how banking will work, and how platform payouts will be recorded. The goal is to know what the LLC will do to your numbers before you start using it.

- hypothetical scenario ↩︎