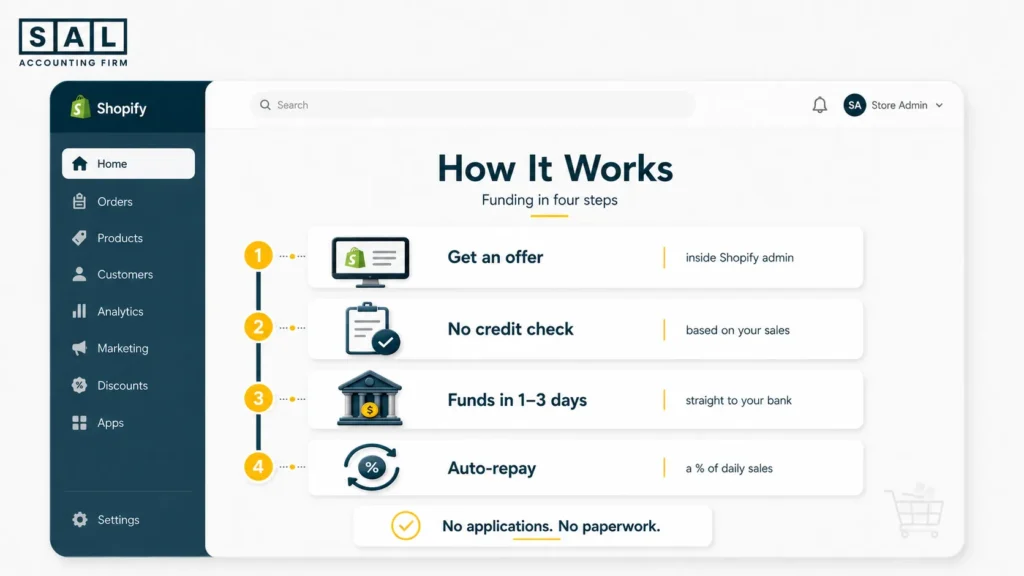

Shopify Capital is funding inside your Shopify admin, up to $2 million, with no credit check. You repay automatically as a percentage of daily sales. Busy days pay more. Slow days pay less.

Need cash for inventory before your busy season, but the bank’s too slow? A lot of store owners hit this wall. In 2025, Shopify Capital funded $4.2 billion, up $1.2 billion. Still, many sellers miss offers. SAL Accounting breaks down the smarter choices.

Talk to our Shopify bookkeeping expert if you’re not sure Shopify Capital is right for your store.

Quick Takeaways

- Shopify Capital funds up to $2 million with no credit check. It looks at your sales, not your credit score.

- You repay as a fixed % of daily sales. Busy days pay more. Slow days pay less or nothing.

- Cost is a factor rate (1.10 to 1.13), not interest. Borrow $50,000 at 1.13 and you pay back $56,500.

- That fee is fixed. It won’t drop if you repay faster.

- Funds land in 1 to 3 business days, right inside your Shopify admin.

- To qualify: 3+ months of steady sales, low refunds, and Shopify Payments.

- Fastest option, but not always the cheapest. RBF lenders like Wayflyer or 8fig can offer more.

See what Shopify’s fees really cost you with our Shopify Fee Calculator before borrowing against your sales.

What Are Shopify Capital Loans and How Do They Work in 2026?

Shopify Capital loans give you quick cash to grow your online store. You can borrow from a few thousand to $2 million based on your sales. They skip credit checks and look at your store’s sales history instead. Funds usually arrive in your bank account within 1 to 3 business days (Shopify fast funding). Use them to cut the starting costs of an e-commerce business.

You repay as a fixed percentage of your daily sales. Busy days mean bigger payments. Slow days mean smaller ones or none. This keeps your cash flow flexible. In 2026, Shopify offers two main types:

- Fixed funding: You get one lump sum and repay it from daily sales. Most must be paid back within 18 months.

- Capital Flex: A revolving line of credit mainly for US merchants. You draw what you need and can borrow again later (Capital flex account).

Quick Example: Your store sells $25,000 in a month. You take a $40,000 advance for inventory. If the repayment rate is 15%, Shopify automatically takes 15% of each day’s sales until the total is paid off.

- Read More: “Shopify Pricing in Canada: The Real Cost of Starting a Shopify Store (Plans, Fees, and Budget Tips)”

Who Can Get Shopify Capital Loans? (Shopify Capital Requirements)

Shopify Capital does not check your personal credit score. Instead, they look at how well your store performs on Shopify. So, consider the best business bank account for your ecommerce store. To qualify, you usually need these things:

- Your store must be open for at least 3 months

- You need consistent sales every month

- You must use Shopify Payments (or an approved payment provider in some countries)

- Your store must have low refund and chargeback rates

- You must follow Shopify’s rules and terms of service

Shopify also looks at your total sales over the past 12 months. Stores with stronger and steadier sales get bigger offers and better terms. Not every store gets an offer. Even if you meet the basics, Shopify’s system decides based on your recent performance. Offers can appear suddenly in your Shopify admin.

Pro Tip: Keep your sales steady and refunds low. Check the Shopify refund policies to avoid surprises. The more consistent your store looks, the more likely Shopify will send you an offer.

Quick Example: A store that sells $15,000–$20,000 every month for 4 months often gets approved for $30,000–$50,000. But a new store with the same total sales but big ups and downs usually gets nothing.

How Much Does Shopify Capital Really Cost? (Shopify Loan Interest Rate)

Shopify Capital does not use a traditional interest rate like a bank loan. Instead, they use something called a factor rate. You must consider it as an expense for your e-commerce store. Let’s explain it in simple terms.

How the Factor Rate Works

The factor rate decides exactly how much extra you pay for the funding (glossary of terms). Here’s how it works:

- You receive a lump sum (for example, $50,000).

- Shopify adds a fee based on the factor rate, usually between 1.10 and 1.13.

- So a $50,000 advance at a 1.13 factor rate means you pay back $56,500 total.

The extra money is the total cost of the funding. This fee stays fixed no matter how fast you repay.

Why the Real Cost Can Change

Your actual cost depends on how quickly you repay the advance. Here’s why it can feel different: You repay daily from your sales, so the effective cost can feel higher or lower depending on how fast you pay it off. Faster repayment usually saves you money in the long run.

Capital Flex works differently. You pay a monthly fee on whatever balance you use instead of one big upfront fee. See how to calculate COGS for e-commerce stores.

Simple Breakdown of Shopify Capital Funding Types

Here’s a quick and easy way to compare the two main options Shopify offers in 2026:

- Fixed funding: You get one lump sum upfront and repay it with a fixed factor fee from your daily sales. Most merchants use this option.

- Capital Flex: This is a revolving line of credit (mainly for US stores). You only pay a monthly fee on the money you actually use, and you can borrow again after repaying.

Many store owners find the total cost reasonable when sales are strong. But if your sales slow down, the daily repayments can eat into your cash flow more than expected.

Pro Tip: Always calculate the total payback amount before you accept an offer. Divide the fee by the amount you receive to see the real cost.

- Also Read: “eCommerce Financial Statements: What They Are, How to Prepare Them, and What They Tell You”

Here’s a detailed comparison of the two Shopify Capital funding options available:

| Feature | Fixed Funding | Capital Flex (US only) | Winner For Most Stores |

| Funding Type | One-time lump sum | Revolving line of credit | Capital Flex |

| Maximum Amount | Up to $2 million | Up to $2 million (updates weekly) | Tie |

| Cost Structure | Fixed factor rate (1.10 – 1.13) | Monthly fee on used balance | Capital Flex |

| Repayment Method | % of daily sales | % of daily sales + monthly fee | Fixed Funding |

| Repayment Flexibility | Medium (fixed term up to 18 months) | High (no fixed term) | Capital Flex |

| Best For | One-time purchases (inventory, equipment) | Ongoing cash flow & seasonal needs | Depends on need |

| Speed of Funding | 1–3 business days | 1–3 business days | Tie |

| Overall Flexibility | Lower | Higher | Capital Flex |

How Does Shopify Loan Repayment Work?

Shopify Capital makes repayment very simple. You don’t send them a monthly check. They automatically take a fixed percentage of your daily sales. Here’s how it works:

- They deduct the money straight from your Shopify Payments balance.

- On busy days, they take more money.

- On slow days, they take less or nothing at all.

- You have no fixed monthly payment to worry about.

Most fixed funding must be paid back within 18 months. Shopify also sets minimum repayment rules. For example, you usually need to repay at least 30% in the first 6 months and 60% in the first 12 months. Check out the guide on cash flow statements for Shopify stores.

If your sales drop for a while, you still owe the full amount, but the daily deductions become smaller. This helps protect your cash flow.

Quick Example: You take a $30,000 advance with a 15% repayment rate. On a day you make $2,000 in sales, Shopify takes $300. On a day you only make $500, they take just $75.

Pro Tip: Track your daily sales closely in the first few months. This helps you predict how fast you will repay the advance.

Tired of dealing with the paperwork and tracking repayments yourself? Leave it all to our accounting and bookkeeping experts.

Pros and Cons of Shopify Capital Loans

Shopify Capital can be a good choice for many store owners, but it is not perfect for everyone. Here’s a simple and balanced look at the real advantages and drawbacks.

The Good Side (Pros)

Shopify Capital has several strong benefits that make it attractive for busy e-commerce owners. Here are the main advantages:

- You get money very fast, often in 1 to 3 days.

- They do not run a credit check.

- Repayments automatically adjust to your daily sales.

- You have no fixed monthly payments, so it feels easier on your cash flow.

- Everything happens inside your Shopify admin, it is very convenient.

- You can get funding even if traditional banks say no.

The Not-So-Good Side (Cons)

Like any funding option, Shopify Capital also has some downsides. Here’s what you should watch out for:

- The total cost can be higher than a regular bank loan.

- If your sales drop, you still owe the full amount.

- Daily deductions can feel painful during slow months (Check Shopify tax exemptions).

- You have limited control over the repayment rate.

- Offers are not guaranteed; Shopify decides who gets them.

- It is not available in every country.

Pro Tip: Shopify Capital works best when your store has steady sales, and you need money quickly for inventory or marketing.

Case Study: How Emma in Toronto Uses Shopify Capital Successfully1

Emma runs a popular handmade skincare brand from her studio in Kensington Market, Toronto. She sells natural beauty products across Canada and keeps steady monthly sales on her Shopify store.

The Problem

Emma needs $45,000 quickly to buy extra inventory before the busy holiday season. Traditional banks move too slowly, and she wants to avoid a long credit check.

What We Do

Emma gets an offer from Shopify Capital. Before she accepts, we check the factor-rate cost against her holiday margins, so she knows the advance still leaves her profitable after fees. We also confirm the daily repayment % won’t squeeze her cash flow once the season slows. The numbers work, so she accepts. The funds land in her bank account within two days.

The Result

Her holiday sales grow by 65%. The daily repayments feel comfortable because her revenue stays consistent. Emma pays back the advance faster than expected and qualifies for a new offer. She now uses Shopify Capital with confidence whenever she needs fast cash for growth, knowing we’ve checked the math first.

Shopify Loan Alternatives: Best Funding Options for Shopify Stores in 2026

Shopify Capital is convenient, but it is not always the best or cheapest choice. Many store owners look for other funding options that offer more flexibility, lower costs, or higher limits. Here are the most popular Shopify loan alternatives that e-commerce businesses use in 2026:

Revenue-Based Financing (RBF)

Companies like Onramp Funds and 8fig specialize in Shopify stores. You repay a small percentage of your future revenue instead of a fixed daily amount.

These options often give higher funding amounts and longer repayment periods. They also help with inventory and ad spending.

Specialist E-commerce Lenders

Platforms like Wayflyer and ClearCo focus only on online stores. They fund marketing campaigns, inventory, or general growth. Approval is fast and based mostly on your Shopify sales data. Check out the Shopify HST/GST based on your sales, too.

Traditional Bank Loans and Lines of Credit

You can apply for a regular bank loan or an SBA loan. These usually have much lower interest rates and longer repayment terms. However, they require good credit, financial documents, and take longer to approve.

Other Working Capital Options

Some lenders offer merchant cash advances or short-term loans from outside Shopify. These can be faster than banks, but sometimes cost more than Shopify Capital.

Quick Comparison:

If you need money super fast and have steady sales → Shopify Capital is great.

If you want lower cost or higher limits → look at revenue-based financing or specialist lenders.

Case Study: How Alex in Mississauga Finds a Better Funding Solution2

Alex owns a growing home fitness accessories store based in Mississauga. His Shopify sales currently reach $35,000 per month as he sells resistance bands, yoga mats, and workout equipment across Ontario.

The Problem

Alex needs $90,000 to launch a big marketing campaign and restock inventory. Shopify Capital only offers him $55,000 at a higher cost, and the daily repayment structure feels risky if sales slow down later.

What We Do

At SAL Accounting, we review his numbers and recommend revenue-based financing from a specialist lender. Alex applies and gets approved for the full $90,000 within one week with much more flexible repayment terms.

The Result

Six months later, Alex’s business grows by 80%. The flexible repayments give him breathing room during slower months, and he pays less overall. He now mixes different funding options depending on his goals and feels much more in control of his cash flow.

Shopify Capital vs Alternatives: Which One Should You Choose?

Now that you know the main options, let’s compare them side by side. This table makes it easy to see the real differences.

| Situation / Need | Shopify Capital | Revenue-Based Financing | Specialist Lenders | Traditional Bank Loans | Best Choice |

| Need money in 1–3 days | Excellent | Good | Good | Poor | Shopify Capital |

| Have steady monthly sales | Excellent | Very Good | Good | Good | Shopify Capital |

| Need $80,000+ for growth | Good | Excellent | Very Good | Good | Revenue-Based Financing |

| Running marketing or ad campaigns | Fair | Very Good | Excellent | Fair | Specialist Lenders |

| Want lowest possible cost | Fair | Good | Good | Excellent | Traditional Bank Loans |

| Sales fluctuate month to month | Fair | Excellent | Good | Poor | Revenue-Based Financing |

| Prefer no credit check | Excellent | Excellent | Excellent | Poor | Shopify Capital or RBF |

| Want maximum flexibility | Good | Excellent | Very Good | Fair | Revenue-Based Financing |

Which one is right for you?

- Choose Shopify Capital if you need money very fast and your sales are consistent.

- Choose Revenue-Based Financing if you want more money and flexible repayments.

- Choose Specialist Lenders if you run ads or sell on multiple platforms.

- Choose Traditional Bank Loans if you have good credit and want the lowest cost.

Many store owners use more than one option at different times. They also consider a series of necessary integrations for Shopify stores.

How to Choose the Right Funding for Your Shopify Store

Picking the right funding can save you time, money, and stress. Here’s a simple way to decide.

1. Look at Your Current Sales

Check your sales first. If your sales are steady every month, Shopify Capital becomes much easier and safer to repay. If you just want to start, choose the best Shopify plan for beginners. Stores with consistent revenue usually get better offers and handle repayments without stress.

Check if your profit can cover the repayments with our Ecommerce EBITDA Calculator.

2. Know Why You Need the Money

Think clearly about your goal. Here are some common situations:

- Need cash in just 2 days for inventory or stock? Shopify Capital is usually a good fit.

- Planning a big ad campaign or long-term growth? Revenue-based financing or specialist lenders often work better.

3. Calculate the Real Total Cost

Always add up everything you will pay back before accepting any offer. Do not just look at the amount you receive. Compare the final cost of Shopify Capital with other options. This helps you avoid surprises later.

4. Consider Mixing Different Options

You do not have to use only one source of funding. Many successful store owners combine options. Here’s how they usually do it:

- Use Shopify Capital for quick, short-term needs

- Use revenue-based financing for larger amounts and better rates

- Combine both when they want both speed and flexibility at the same time

Our experienced ecommerce accountant can help you build the right mix that supports your growth without straining your cash flow.

Is Shopify Capital the Best Funding Option for Your Store in 2026?

Shopify Capital loans give you fast cash without any credit checks. They feel convenient for many store owners. But they work best when your sales stay steady. Take time to compare Shopify Capital with other funding options like revenue-based financing and specialist lenders. The right choice depends on your sales, your goals, and how much flexibility you want.

Many successful store owners mix different funding sources. This helps them grow smarter. Pick the one that truly supports your business and keeps your cash flow healthy. If you need help deciding the best funding option for your store, book a free consultation with SAL Accounting today.