Our goal is to show you how to open a US bank account from Canada in 2026. We want to make cross-border banking easier and cheaper, whether you visit the US a lot, own property there, or do business across the border. The surprising part is that most Canadians miss this one big thing: without a US account, you pay sneaky currency conversion fees and bad exchange rates on every transaction. That can add up to thousands of dollars a year.

We’ll explain exactly why this happens and how to stop it. This guide covers clear steps, practical tips, and how SAL Accounting can help.

Quick Takeaways

- anadians can open a US bank account remotely in 2026—no US visit, SSN, or address always required.

- A US account saves thousands yearly by avoiding 2.5% foreign transaction fees and poor exchange rates.

- Wise Multi-Currency Account provides the fastest 100% online setup with real US routing and account numbers plus no monthly fees.

- Report US accounts over $10,000 (FBAR) and foreign assets over CAD $100,000 (T1135) to stay compliant and avoid fines.

- Cross-border options like multi-currency or borderless accounts make transfers, payments, and USD holding simple and low-cost.

Can a Canadian Open a US Bank Account?

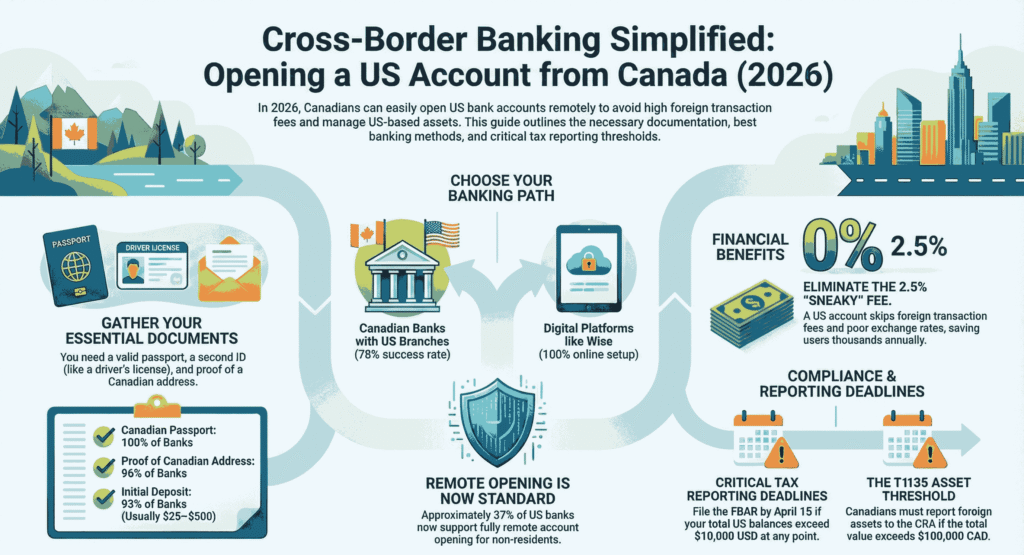

Yes, Canadians can open a US bank account. Many easy options exist, especially through Canadian banks with US branches like RBC Bank, TD Bank, or BMO. You can often apply online or from Canada, no US address or Social Security number needed. You just need to be 18 or older, show ID like your passport and driver’s license, and provide proof of your Canadian address. Our cross -border tax accountant can help you handle the process with ease.

Why Do Canadians Need US Bank Accounts

Before we jump into the “how,” here’s why a US bank account actually makes sense for many Canadians:

- Traveling or spending time in the US feels smoother. You can withdraw cash, pay bills, or shop without relying on Canadian cards.

- You skip the annoying 2.5% foreign transaction fees on US purchases and save money right away.

- Paying your US mortgage, property taxes, and bills becomes way easier, no extra steps or high conversion costs.

- You can receive payments directly in US dollars from clients, employers, or sales, with no delays or bad exchange rates.

- It’s an easy first step to start building a US credit history for things like future loans or mortgages.

Fun fact: According to NAR, more than 1 in 4 foreign property owners in Florida are Canadian, and having a local bank account makes managing these investments much easier.

Read More: “Canada-US Cross-Border Personal Loans: 2026 Tax Implications“

Step-by-Step Process: How to Open a US Bank Account from Canada

Here’s a simple guide to opening a US bank account as a Canadian in 2026. The process is easier than you might think. We’ll cover the clearest, most reliable steps so you can get set up quickly and avoid common mistakes:

Step 1: Figure Out What You Need

First, think about what you need your US account for: Will you mainly use it for travel, property, or business? How often will you need to get to your money in the US? Do you want it to connect with your Canadian accounts? Your answers will help you pick the right bank and account type. Check the best US banks for Canadians before anything.

Step 2: Requirements for Opening a US Bank Account

As a non-resident opening a US bank account, you’ll need these papers:

| Document | Required by | Notes |

| Canadian passport | 100% of banks | Must be valid |

| Second photo ID | 87% of banks | Canadian driver’s license works great |

| Proof of Canadian address | 96% of banks | Recent utility bill or bank statement |

| US mailing address | 74% of banks | Can use a friend’s address or mail service |

| Money for first deposit | 93% of banks | Usually $25-$500 depending on the account |

| SSN or ITIN | 58% of banks | Many banks don’t ask Canadians for this |

Pro Tip: Call the bank before you visit to check exactly what they need. Each bank has its own rules, and these can change—some might even ask for a quick face scan with 2026’s new tech rules.

Step 3: Pick the Right Bank

Some US banks are friendlier to Canadians than others. Our corporate tax experts recommend considering these options based on your specific needs:

- TD Bank: Perfect if you already use TD Canada Trust

- RBC Bank USA: Made specially for Canadians with US banking needs

- BMO Harris: Great choice if you’re a Bank of Montreal customer

- Chase: Huge network if you need access all over the US

- Bank of America: Popular with Canadians buying property in southern states

Example: Sarah from Toronto visits Florida every winter. She picked TD Bank because she already has a TD Canada Trust account. She can see both accounts in one app and move money between them right away.

➜ Read more: “Taxes for US Citizens Working Remotely for Canadian Companies”

Step 4: Visit a Branch (If You Can)

For the easiest experience:

- Call ahead to make an appointment

- Bring all your documents

- Take your first deposit with you

- Fill out the forms with a bank employee

- Set up online banking while you’re there

- Ask for a debit card and checks if you need them

The whole process usually takes 1-2 hours, and your account will be ready to use within 1-3 days.

How to Open a US Bank Account Online as a Non-Resident

Many banks now let Canadians open accounts fully online or remotely. In 2026, around 37% of options support this convenient process, no branch visit required.

Digital Banking Options

Here’s a quick look at the best online-only choices for Canadians opening a US bank account remotely. These let you handle everything from your phone or computer:

Wise Multi-Currency Account

The Wise Multi-Currency Account lets you sign up 100% online in about 20 minutes and provides real US bank details, like routing and account numbers. It has no monthly fees (just small conversion costs) and includes a debit card for US ATMs and shopping, with the whole process taking around 20 minutes. Banks use extra security like two-step logins now, so it’s safe too.

Mercury (For Businesses)

Mercury is made for international businesses. It offers full US banking features with checkbooks, no monthly fees or minimum balances, and a simple online application with document upload. Approval time is usually 7-10 days. You may only need to get a TIN for your business and US bank account.

Pro Tip: When applying online, make sure your documents are clear and exactly match what’s asked for. Most rejections happen because of blurry or wrong documents.

Using Canadian Banks with US Branches

If you already bank with these Canadian banks, you’ve got a big advantage with cross-border banking solutions for Canadians:

- TD Canada Trust → TD Bank: Start your application at your Canadian branch

- RBC → RBC Bank USA: Cross-border packages available

- BMO → BMO Harris: Connected cross-border banking

- CIBC → CIBC US: Special cross-border services

These cross-border relationships usually offer a simpler application process and better approval chances, with a 78% success rate compared to 42% for other methods. They also make money transfers between your Canadian and US accounts easier. Plus, you get one online view for all your accounts, keeping everything in one spot.

Case Study: Liberty Village Remote Business Owner Streamlines Cross-Border Payments1

The Problem: Jennifer from Liberty Village in Toronto reaches out about her marketing business. “I have three big US clients, but I’m losing about 4% on every payment with my current setup,” she says. “Last month I lost over $900 in fees on $25,000 of income.”

What We Do: We suggest a Wise Multi-Currency Account instead of a traditional bank. We guide her through the application together and upload her ID plus a recent utility bill for proof of address. “It’s so quick—nothing like dealing with normal banks,” she tells us.

The Result: In just 2 days, Jennifer gets her US account details and starts billing clients immediately. “The first payment comes through the next day with no fees,” she says. She now saves around $850 every month. Her US client list grows by 40%, and she keeps money in USD for expenses without constant conversions.

➜ Read more: “How to Register a Business in the US from Canada: Full Guide“

What Are Different Types of US Bank Accounts for Canadians?

Canadians pick US accounts based on needs like spending, property, or business. Main types include checking for daily use, savings for interest, and multi-currency accounts for easy cross-border transfers. The right choice cuts fees and simplifies US money management. Here’s a quick breakdown:

Checking Accounts

Checking accounts are the most common and useful option for Canadians. They’re perfect for everyday transactions and paying bills, and they come with a debit card for shopping and ATMs, though wire transfers can cost $30-50. The monthly fee is $8-15, often waived if you keep enough money in it.

They’re best for people who travel to the US often or own property there. See the process for cross-border real estate transactions.

Savings Accounts

Savings accounts are great for keeping money and earning some interest. They earn 0.5-4.25% APY on your balance as of March 2026, though US rules limit you to 6 withdrawals per month. The monthly fee is $5-10, often waived.

They’re best for keeping US dollars for future use or investment.

Business Accounts

Business accounts suit Canadians doing business in the US. They keep your business and personal money separate and might need a US business entity like an LLC or Corporation, plus an EIN (Employer Identification Number). The monthly fee ranges from $15-50. If you’re considering establishing a business in the US.

They’re best for Canadian businesses with US customers or operations.

Example: A Toronto tech company opened a Mercury business account to accept payments from US clients. The process took 18 days but saved them the 3.5% fees they were paying on cross-border transactions.

Read More: “Global Minimum Tax: How Pillar Two Tax Affects Canada–U.S. Cross-Border Payments“

| Account Type | Best For | Key Features | Monthly Fees | Interest (2026 APY) | Notes |

|---|---|---|---|---|---|

| Checking Accounts | Daily use, travel, property payments | Debit card, bill pay, ATM access | $8–$15 (waivable) | Usually 0% | Wire fees $30–$50; ideal for frequent US use |

| Savings Accounts | Holding USD, earning interest | Interest on balance, secure storage | $5–$10 (waivable) | 0.5%–5.00% | Withdrawal limits may apply |

| Business Accounts | US clients, cross-border operations | Separate funds, ACH/wires, invoicing | $15–$50 | Varies/low | Often needs US entity + EIN; Mercury popular |

Tax Implications of a US Bank Account for Canadians

A US bank account creates several tax obligations for Canadians. You must report the account to the CRA, file US forms like FBAR if balances exceed thresholds, and properly declare any interest income to stay compliant and avoid penalties. Here’s what you need to know in 2026:

Canadian Tax Obligations

Let’s start with what Canada expects from you when you have a US account.

Report All Income

Any interest you earn in your US account must be reported on your Canadian tax return. For example, $200 USD interest earned equals about CAD 270 to report—watch for exchange rate gains too.

T1135 Foreign Income Verification

The T1135 form is needed if your total foreign assets go over CAD 100,000. It’s due with your tax return. Penalties can hit up to 5% of the asset value if you don’t file. Check out the Guide for filling the Form T1135.

US Tax Considerations

Now, here’s what the US side wants you to know.

W-8BEN Form

The W-8BEN form shows you’re not a US person. It cuts withholding tax on interest from 30% to 10%. File it when opening your account and every 3 years after. Se how to file Form W-8BEN as a foreign individual.

Foreign Bank Account Report (FBAR)

You need this if your US accounts total more than $10,000 at any point. Banks also report deposits over $10,000 separately. It’s filed with the US Treasury’s Financial Crimes Enforcement Network. The deadline is April 15, with an automatic extension to October 15.

Pro Tip: Pro Tip: Submit Form W-8BEN when opening your US account to certify non-US status and reduce withholding tax on interest or dividends under the Canada-US tax treaty (often to 0% on interest or 15% on dividends).

Case Study: Mississauga Snowbird Couple Avoids Cross-Border Tax Headaches2

The Problem: Robert and Maria from Mississauga called after buying a winter home in Arizona. “We were paying over $3,200 a year just in foreign transaction fees,” Robert says. “We sent $95,000 USD for home updates, and our accountant mentioned FBAR forms we’d never heard of,” adds Maria.

What We Do: We explain the tax forms they need to file. Their US account exceeds the $10,000 limit for FBAR reporting, and their foreign assets are above the CAD $100,000 threshold for the T1135 form. We show them how to report interest income, connect them with our tax expert, and help fill out forms to reduce their withholding tax rate from 30% to 10%.

The Result: By sorting out their tax situation, they avoid potential fines that could exceed $10,000. We recommend RBC Bank USA for smoother cross-border banking. “Just having peace of mind was worth it,” Robert tells us. “We’re saving about $4,700 a year on fees and taxes.” They now manage their money easily and have recommended our help to five other Canadian snowbird couples.

➜ Read more: “Factual vs. Deemed Residency for Taxes in Canada: Key Differences“

Common Challenges When Opening a US Bank Account as a Canadian

Even well-prepared Canadians often face hurdles like paperwork issues, address rules, or tax form confusion. Here are the top challenges in 2026 and easy fixes to avoid delays or rejections:

1. US Address Requirement

Many US banks (around 74%) require a physical US address for account opening, which often stops non-residents at the start. Here are the practical solutions:

- Use a friend or family member’s US address (get their permission first!)

- Use a property you own in the US

- Sign up for a mail forwarding service ($10–25/month)

- Pick banks with Canadian-specific programs that don’t require a US address

2. SSN or ITIN Requirement

Some banks demand a US tax ID like an SSN or ITIN, which creates a barrier for most Canadians. The easy fixes are: choose banks that waive it for Canadians (like TD, RBC, and about 42% of others), apply for an ITIN using Form W-7 (takes 7–11 weeks), or use your existing Canadian banking relationship for extra verification.

3. No US Credit History

Certain banks check US credit and may reject applicants with no history in the US. You can get around this by providing your Canadian credit report (with translation if needed), getting a reference letter from your Canadian bank, or opening a basic account first to start building US credit over time. Our cross-border personal tax accountant helps you avoid any mistakes.

Example: When Michael from Toronto needed a US account for his Florida vacation home, Chase initially refused due to no US credit history. He brought a letter from RBC and his Canadian credit report, and the branch manager approved it on the spot.

➜ Read more: “7 Canada US Tax Treaty Benefits You Need to Know“

Final Words

Opening a bank account in the US as a Canadian (or any foreigner) is simple with some prep. A US bank account for Canadian residents cuts fees and makes travel, property, or business easier—with demand up 32% this year, says SAL Accounting. Check the requirements for opening a US bank account, as each bank varies slightly.

You can open a US bank account online non resident or in person—follow this guide on how to open a US bank account from Canada. It’s perfect for a non-resident bank account in the USA. For personal help, book a free chat with SAL Accounting, we’ll find the best solution for you!

Frequently Asked Questions

Yes, Canadians can open US bank accounts remotely through online platforms like Wise or by using Canadian banks with US branches (TD, BMO, RBC). The success rate for remote applications is around 78% for Canadians, much higher than for other foreigners.

TD Bank is usually the best choice for most Canadians because of its many branches, connection with TD Canada Trust, and simpler documentation requirements. For online-only options, Wise offers the easiest setup with no monthly fees.

While 74% of US banks ask for a US address, it doesn’t need to be your main home. You can use a friend’s address, a property you own, or a mail forwarding service. Some banks that focus on Canadian customers have found ways around this requirement.

You’ll need your Canadian passport, a second ID (like a driver’s license), proof of Canadian address (utility bill or bank statement), and sometimes a US mailing address. Some banks might also ask for an SSN/ITIN, though many don’t require this from Canadians.

Yes. Canadians with US accounts may need to file an FBAR if their US assets go over $10,000 at any point during the year. Also, interest earned is taxed in both countries (with treaty benefits cutting US withholding to 15%), and accounts over CAD $100,000 must be reported on the T1135 form to the CRA.