The U.S.-Canada tax treaty reduces or eliminates withholding tax on dividends, interest, royalties, and pensions for cross-border residents. Our goal is to make these rules clear and help you pay the lowest possible U.S. withholding tax as a Canadian (or Canadian tax on U.S. income). Most Canadians and cross-border investors lose $10,000+ every year because they never claim the treaty’s lower rates. One simple form cuts the default 30% U.S. withholding tax to 0–15%.

In this guide, we at SAL Accounting will reveal exactly how Canada’s tax treaty with the US works and how you claim every dollar you deserve.

Quick Takeaways

- The U.S.-Canada tax treaty cuts default 30% withholding tax to 0–15% on dividends, interest, and royalties.

- File Form W-8BEN or NR301 before payments to claim reduced U.S.-Canada tax treaty withholding rates.

- Under the Canada tax treaty with the US, interest is 0%, royalties 0–10%, dividends just 15% (or 5%).

- Canadians avoid excess US withholding tax on Canada-sourced income with one timely form.

- Renew W-8BEN every 3 years or lose your U.S.-Canada tax treaty withholding rates instantly.

What is Withholding Tax Under the U.S.-Canada Tax Treaty?

Withholding tax is the tax taken straight from certain types of income, like dividends or interest, paid across borders. The U.S.-Canada tax treaty helps reduce or even remove this tax. It depends on the type of income and where the payee lives. The treaty’s goal is to prevent double taxation and ensure fair treatment for taxpayers.

- → Example: A Canadian company receiving U.S.-Canada dividend withholding tax from a U.S. business would normally face a 30% withholding tax. However, the treaty reduces it to 15%. This allows the company to keep more of its earnings.

Ask our cross-border tax experts for help and save more money in the long run.

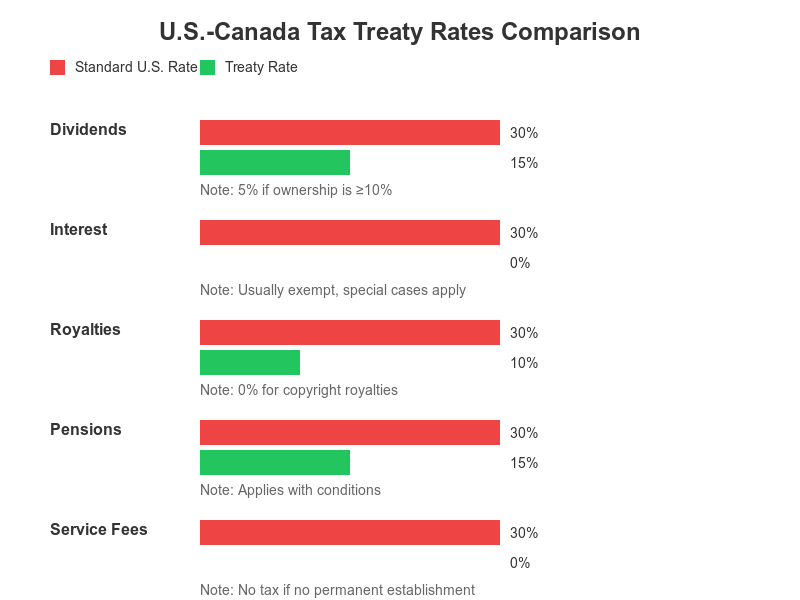

How Are the U.S. Canada Tax Treaty Withholding Rates?

The U.S.-Canada tax treaty helps cut down or even remove withholding taxes on certain types of income. Here’s a chart comparing the usual U.S. withholding tax rates with the lower rates under the treaty:

For complete details about these treaty rates and additional scenarios, check IRS Publication 597 which is about United States-Canada income tax treaty.

- → Example: A Canadian tech company earning royalties from a U.S. company would usually pay a 30% withholding tax. But by filing the right forms (like Form W-8BEN), they can bring it down to 0%, saving a lot on taxes. In my experience, this gets easily accepted without any issues as long as it’s done correctly.

Current U.S.-Canada tax treaty withholding rates in 2025 are as follows:

| Income Type | Default Rate (no treaty) | Treaty Rate for Canadian Residents | Treaty Rate for U.S. Residents |

| Dividends (general) | 30% | 15% | 15% |

| Dividends (≥10% corporate ownership) | 30% | 5% | 5% |

| Interest | 30% | 0% | 0% |

| Royalties – Copyright / artistic | 30% | 0% | 0% |

| Royalties – Industrial / commercial | 30% | 10% | 10% |

| Pensions & annuities (periodic) | 30% | 15% or 0% | 15% or 0% |

| Social Security benefits | 30% | 0% (U.S. → Canada) | 0%–25.5% (Canada → U.S.) |

- Read More: “Tax Treaty Between the United States and Canada”

How to Use the U.S.-Canada Tax Treaty to Reduce Withholding Taxes

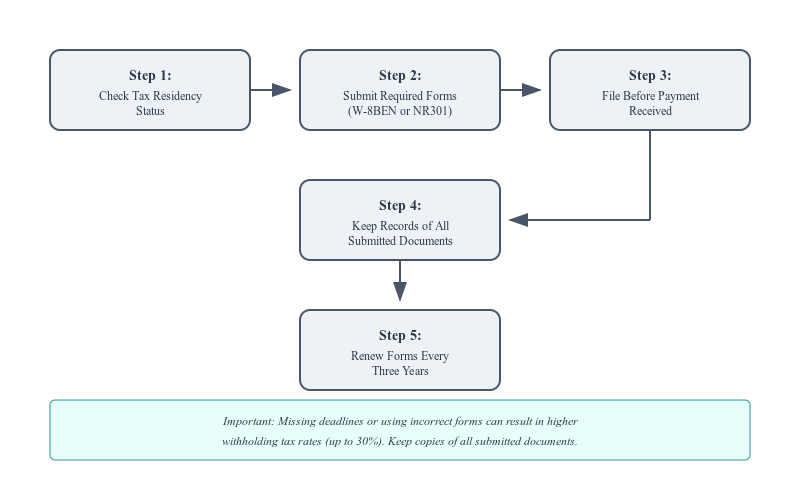

There are some specific steps you need to take in order to lower your withholding tax with the U.S.-Canada tax treaty. Here we explain these steps:

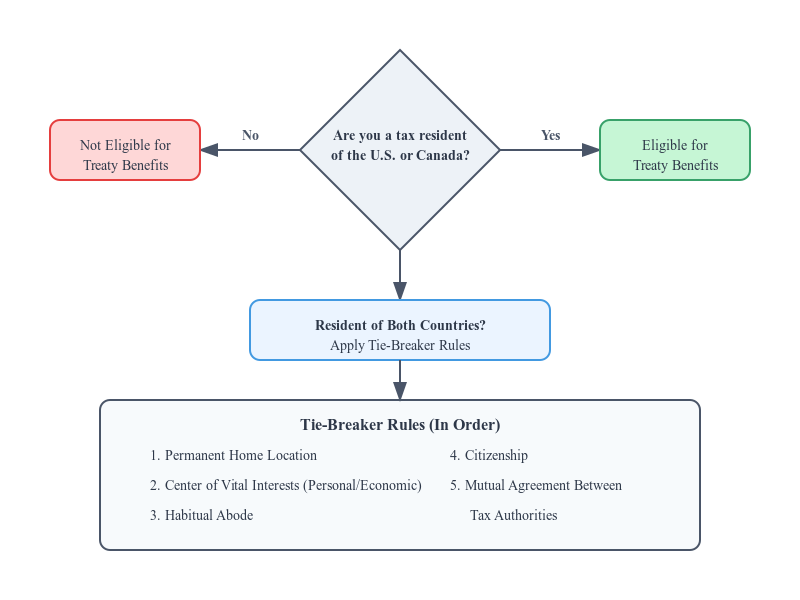

1. Check If You Qualify for Treaty Benefits

To get lower withholding rates, you must be a tax resident of either the U.S. or Canada. According to CRA’s guidelines on determining residency status, your residency status determines your eligibility for treaty benefits. If you’re a resident of both, tie-breaker rules determine your main residency.

- Note: If you’re a tax resident in both countries, tie-breaker rules will decide your main residency. They look at where you live, work, spend the most time, have the strongest ties, and your citizenship.

2. Submit the Required Documentation

To get the lower tax rates under the treaty, you’ll need to submit a few forms. Here are the main ones:

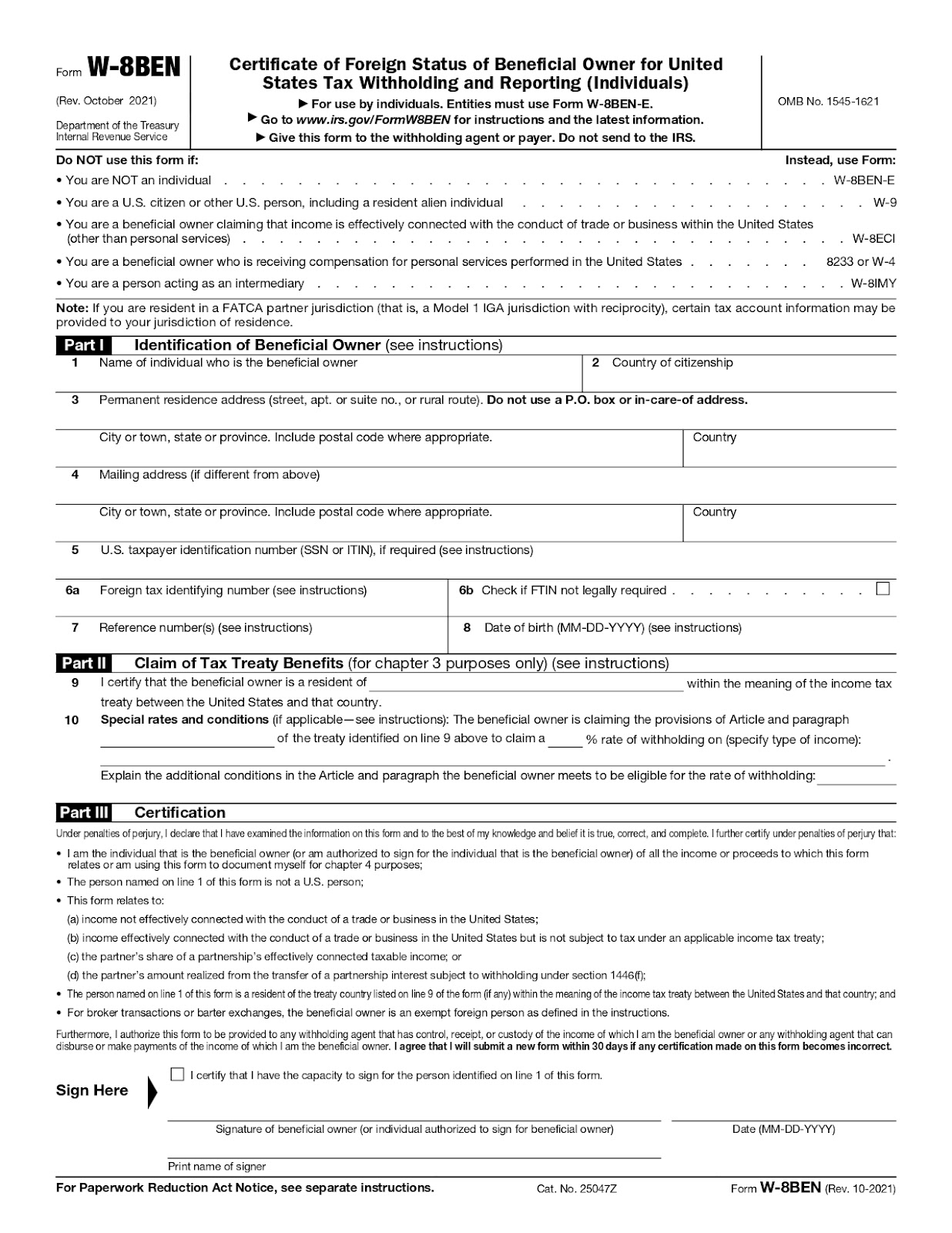

Form W-8BEN (Individuals) or W-8BEN-E (Entities)

These forms show that you’re a non-U.S. taxpayer and help you claim the reduced tax rates.

- Pro Tip: IRS Form W-8BEN for Canadians lasts for three years, so remember to renew it. Send it to the U.S. payer before they make any payments (like on dividends and royalties) to get the lower tax rates. In my opinion, most businesses forget to do this every 3 years, so best to keep a reminder on your phone.

Form W-8 BEN; Rev. October 2021 Form W-8 BEN; Rev. October 2021 |

- Download the official Form W-8 BEN here. Also you can visit the IRS website if you are looking for more information.

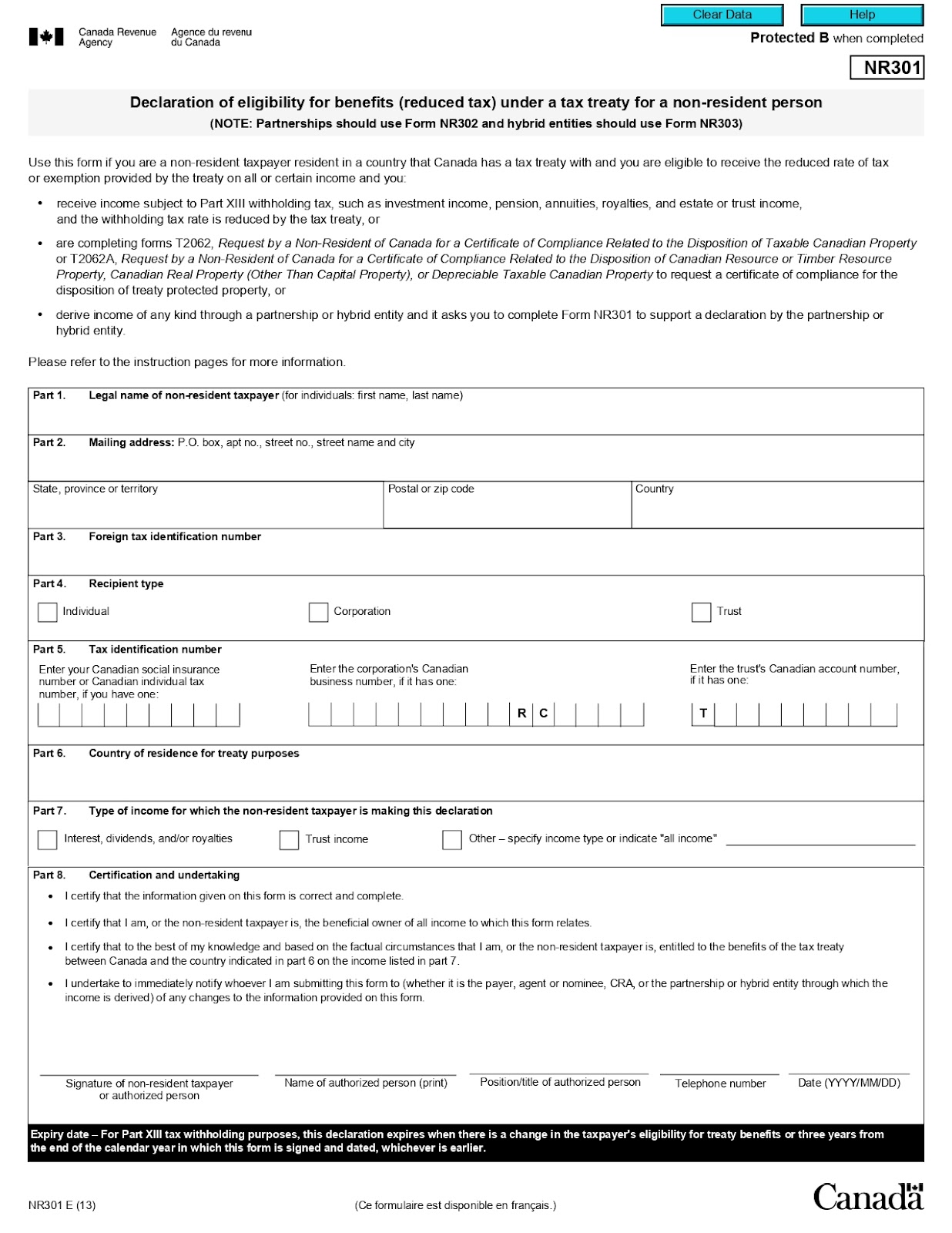

Form NR301

If you’re a U.S. resident getting Canadian income, use this form to claim the treaty’s lower rates (like 15% on Canadian dividends). It helps make sure the correct tax rate is applied so you don’t get stuck with the higher U.S. rates.

Form NR301; Declaration of eligibility for benefits (reduced tax) under a tax treaty for a non-resident person Form NR301; Declaration of eligibility for benefits (reduced tax) under a tax treaty for a non-resident person |

- Download the official Form NR301 here. Also you can visit the CRA website if you are looking for more information.

Form 8833

Form 8833 is needed if you’re claiming special treaty benefits. It tells the IRS your treaty position.

3. Timing and Filing Process

To make sure you get the reduced tax rates, timing is key. Here’s what you need to keep in mind:

File Before Receiving Payment

In order to use tax treaties to reduce withholding rates, make sure you submit the forms before you get paid. Filing late means the higher withholding tax will apply. Plan ahead to ensure the lower rates take effect.

Documentation Updates

Forms like W-8BEN are valid for three years. Be sure to update them regularly to keep the reduced withholding tax.

Case Study: Tax Optimization for a U.S. Investor in Yorkville, Toronto1

The Issue: A U.S. investor living in Yorkville, Toronto loses $10,000 because their tax forms are filed late. As a result, the payer applies a 25% withholding tax on Canadian dividends instead of the reduced 15% rate available under the Canada-U.S. tax treaty.

The Solution: We submit Form NR301 (Declaration of Eligibility for Benefits Under a Tax Treaty for Non-Resident Persons) and Form W-8BEN (Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting) well before any dividends are paid to the investor. We also instruct the client to keep these forms current by renewing the W-8BEN every three years to maintain continuous eligibility for the lower treaty rate.

The Outcome: By filing the forms on time, the investor saves 10% in withholding tax on every dividend payment. Ongoing renewals ensure the preferential 15% rate remains in place indefinitely, eliminating future avoidable tax leakage and helping preserve and maximize after-tax returns for their portfolio managed from Yorkville, Toronto.

Common Scenarios and How to Use US Withholding Tax in Canada

These are a few situations where you can use the tax treaty to lower cross-border withholding taxes in Canada. Here’s how it works:

Scenario 1: A Canadian Consultant Working with U.S. Clients

If you’re a Canadian consultant working with a U.S. client, you can avoid the 30% withholding tax by filing Form W-8BEN. This form shows you’re a foreign taxpayer and gets you the 0% withholding tax rate. Check the complete guide for filing Form W-8BEN. The benefits are:

- Savings on the 30% tax

- More of your payment

- Easier tax reporting

- Access to other benefits (e.g., lower taxes on royalties or fees)

Scenario 2: U.S. Investor Getting Canadian Dividends

A U.S. investor getting dividends from a Canadian company can file Form NR301. This will reduce the withholding tax from the 25% Canadian domestic rate to the 15% treaty rate. The benefits are:

- 10% tax savings and more dividend

- Lower treaty rate vs. higher Canadian rate

- Correct tax treatment with treaty benefits

- Other treaty benefits (dividends, interest, etc.)

- Read more: 7 Canada US Tax Treaty Benefits You Need to Know

- Read more: “7 Canada US Tax Treaty Benefits You Need to Know”

Canada Tax Treaty with US: Common Mistakes to Avoid

Avoiding mistakes helps you get the most out of the U.S.-Canada tax treaty and avoid extra taxes. Here are the biggest ones and how to fix them:

| # | Mistake | Consequence | Quick Fix |

|---|---|---|---|

| 1 | Filing forms late | 30% withholding instead of 0–15% | Submit W-8BEN/NR301 2–3 weeks early |

| 2 | Wrong form | Full 30% tax | W-8BEN/E → U.S. income; NR301 → Canadian income |

| 3 | Errors on form | Form rejected, 30% applied | Verify name, TIN, residency & income type |

| 4 | No residency proof | Treaty denied | Attach CRA residency certificate or IRS 6166 |

| 5 | Forgetting to renew (every 3 yrs) | Reverts to 30% next day | Calendar reminder → renew before Dec 31 yr 3 |

| 6 | No records kept | Audit risk + penalties | Save all forms, certificates & 1042-S/NR4 |

1. Missed Deadlines

Filing forms late can cost you. Without the right forms submitted before payment, you could face higher taxes. For example, if Canadian contractors don’t give U.S. companies Form W-8BEN, the companies have to keep 30% of the payment for taxes. That’s a lot to lose.

The fix is easy. Send your forms before you get paid. It takes time to process, so try to file them 2–3 weeks early. If you’re late, you’ll have to ask the IRS or CRA for a refund, and that can take months..

2. Using the Wrong Form

Each income type needs a specific tax form. Using the wrong one can cost you treaty benefits and push your tax rate up to 30%. For instance, filing Form NR301 for U.S. royalties will skip the 0% rate and leave you paying 30%.

Always try to match your form to your income:

- Form W-8BEN – For dividends, interest, and royalties.

- Form NR301 – For U.S. residents earning Canadian income.

- Form 8833 – To claim treaty benefits.

Double-check factual vs. deemed residency for taxes in Canada, tax ID, and income type before filing. A small mistake can cost you thousands.

Case Study: Cross-Border Dividend Tax Savings for a U.S. Investor in The Annex, Toronto2

The Issue: A U.S. investor living in The Annex, Toronto faces a $10,000 loss because their tax forms are filed late. This causes a 25% withholding tax on their Canadian dividends instead of the reduced 15% rate available under the Canada-U.S. tax treaty.

The Solution: SAL Accounting steps in. We file Form NR301 and Form W-8BEN before the dividends are issued. The team also renews the W-8BEN every three years to ensure the investor keeps the lower treaty rates in place.

The Outcome: The investor saves 10% on withholding tax and avoids future losses by staying up to date. Ongoing compliance secures the preferential 15% rate indefinitely, protecting their net returns on Canadian dividend income from their portfolio managed in The Annex, Toronto.

3. Filling Out Forms Incorrectly

Even small mistakes—like a missing tax ID, residency status, or income type—can invalidate your form. If this happens, you could lose U.S.-Canada tax treaty benefits and face the default 30% tax rate instead of a lower one.

It’s essential to double-check everything before submitting. Make sure your name, tax ID, residency details, and income type are correct. Need help with your US tax forms? Contact our US tax accountants to ensure proper documentation and compliance.

- Pro Tip: IRS and CRA reject thousands of forms every year due to errors. Avoid the hassle—take a few extra minutes to review your details.

4. Not Keeping Proof of Residency

To qualify for the U.S.-Canada tax treaty benefits, you must prove your residency. Without proper documents, tax authorities may reject your claim and apply higher taxes.

If you’re a Canadian resident claiming treaty benefits on U.S. income, get a Tax Residency Certificate from the CRA. Reporting foreign business income in Canada is always a must. If you’re a U.S. resident receiving Canadian income, you’ll need proof from the IRS.

- Pro Tip: Always submit your residency certificate with your tax forms. This prevents delays and makes sure the lower tax rate applies.

5. Forgetting to Renew Forms

Forms like W-8BEN expire every three years. If you forget to renew, the withholding agent must apply the higher tax rate by default.

It’s a good idea to set a calendar reminder to renew your forms before they expire. This keeps your tax rate low without interruptions.

- Example: A U.S. investor receiving $20,000 in Canadian dividends forgot to renew Form NR301. This mistake cost them an extra $2,000 in taxes because they were charged 25% instead of 15%.

6. Not Keeping Records

Even if you submit everything on time, failing to keep copies can be a problem later. If the IRS or CRA asks for proof, missing documents could mean paying higher taxes.

Keep a dedicated folder (digital or physical) for:

- All submitted tax forms

- Residency certificates

- Email confirmations from withholding agents

- Payment receipts

Audits happen. Keeping records makes it easy to prove your treaty benefits and avoid unnecessary taxes.

Final Thoughts

The U.S.-Canada tax treaty helps you pay less tax and avoid double taxation on cross-border income. Filing the right forms and keeping records can save you money and prevent tax issues.At SAL Accounting, we make cross-border taxes simple. Our experts help you maximize savings and stay compliant. Contact us today and book your FREE consultation.

FAQs on U.S. Withholding Taxes

It’s a tax taken from payments like dividends, interest, and royalties before you receive them. The U.S.-Canada tax treaty helps lower these taxes based on the type of income.

To reduce or avoid U.S. withholding tax, Canadians need to check if they qualify for treaty benefits, file the right form (W-8BEN for individuals or W-8BEN-E for businesses), prove they live in Canada for tax purposes, and submit the forms before getting paid.

The treaty lowers taxes on U.S. income for Canadians. Dividends are taxed at 15%, or 5% for certain shareholders. Interest is tax-free. Royalties are 0% for copyright-related payments and 10% for other types.

The treaty lowers withholding taxes and allows tax credits, so you don’t get taxed twice on the same income. It also sets rules on which countries can tax different types of earnings and includes special rules for pensions and social security.

This form proves you’re not a U.S. taxpayer and lets you claim treaty benefits. If you earn U.S. income, you need to file it to get lower tax rates. It expires every three years, so you’ll need to renew it.

Yes. If too much tax was taken, you can apply for a refund. For U.S. taxes, file Form 1042-S and Form 1040-NR. For Canadian taxes, use Form NR7-R to get back any extra withholding tax.