If you’re a Canadian business owner earning income from foreign markets, you’re part of a thriving network of global entrepreneurs with huge growth opportunities. The latest data indicates that Canadian businesses hold over CAD$1.5 trillion in foreign direct investments, with 45% of small businesses engaged in international trade. In fact, as of August 2024, Canadian investors have invested $12.3 billion in foreign businesses.

As intriguing as the growth may sound, there is a critical obligation to understand how to report foreign business income in Canada. Each year, the CRA processes over 200,000 Form T1135 submissions, a key requirement for foreign income reporting. To get started, you must first gather statements for your income and tax payments and complete the necessary forms, like Form T1135. After that, check whether you’re eligible for a foreign tax credit. If you have all the required information, you’re ready to file your tax return with the CRA.

Ready to learn how to report foreign business income in Canada? In this article, I will walk you through a step-by-step process, and you’ll see that reporting your foreign business income is not so difficult after all!

Key Takeaways

Step-by-Step Process: Canadians can buy a business in the US by following six essential steps: choosing a state, understanding visa requirements, obtaining an ITIN, preparing licenses and permits, drafting a Letter of Intent (LOI), and closing the deal.

Visa Options: The E-2 Treaty Investors Visa and the EB-5 Immigrant Investor Visa are popular options for Canadians, offering different requirements and benefits depending on investment size and business involvement.

Tax and Legal Considerations: Canadians must navigate both federal and state regulations. Professional legal and tax advice is essential for compliance and smooth operations.

State Selection: Different US states offer various advantages, such as tax policies, business regulations, and market potential. Florida, Texas, Nevada, and California are common choices with specific benefits and challenges.

Due Diligence: Thorough research on financial health, market position, and potential risks of the business is critical to ensure profitability and alignment with business goals.

Business-Friendly Environment: The US provides lower corporate taxes, a stable economy, and supportive regulations, making it a prime location for Canadian investors.

Financing and Loans: Canadians can secure financing in the US, though conditions such as ownership percentages may apply. Building credibility with US banks is key to securing loans.

Legal Assistance: While not mandatory, hiring a lawyer is advisable to navigate complex legal and regulatory requirements and ensure a smooth purchase process.

Table of Contents

Understanding Foreign Business Income for Tax Reporting

Residents of Canada are subject to the taxation of their income earned worldwide. This includes employment or owning a business in a foreign country or owning property outside of Canada.

Your received income should be converted to Canadian dollars, often according to the Bank of Canada, on the date you have earned it. If the currency in the foreign country you have a business in does not fluctuate constantly, you may use the average of the rate for taxation purposes. The Canada Revenue Agency (CRA) also approves the rate driven by Bloomberg L.P., Thomson Reuters Corporation, and OANDA Corporation.

Before answering how to report foreign business income in Canada, let’s see what business income is. It is any income you receive from a profession, a trade, or pursuing any trade-like action to gain profits. There also must be evidence to support your intention. Keep in mind that business income is entirely different from employment income.

So, for example, your wage or salary in the US is not subject to business income tax unless you are a worker or employee of a particular company or organization.

The Role of Tax Treaties in Canada’s International Trade

Tax treaties in Canada, AKA double-taxation agreements (DTA), serve as agreements between Canada and other countries to prevent double taxation and encourage investment and trade across borders.

Tax treaties define how an income must be taxed if earned outside of the country you reside in. They can also provide you with the procedure framework and proper resolutions. They can even sometimes help particular organizations and individuals be excused from paying taxes. But most importantly, they are responsible for determining whether you are eligible to receive a foreign tax credit.

In Canada, we now have tax treaties with over 90 countries, ensuring you don’t get taxed twice in both countries. Some of the Canadian tax treaties with major business trading partners include:

1.United States (US-Canada Tax Treaty)

- Withholding dividends tax: 15% (5% for corporate shareholders owning at least 10% of the company).

- Withholding tax on interest: Generally exempt under treaty provisions.

- Business profits: Taxed in the source country only if the business has a permanent establishment there.

2.United Kingdom (UK-Canada Tax Treaty)

- Withholding dividends tax: 15% (5% for substantial corporate shareholders).

- Withholding tax on royalties: 0% for most cases.

- Business profits: Taxed in the source country based on permanent establishment there.

3.China (China-Canada Tax Treaty)

- Withholding tax on dividends: 10%.

- Withholding tax on royalties: 10%.

- Business profits: Taxable only if there is a permanent establishment.

4.India (India-Canada Tax Treaty)

- Withholding tax on dividends: 15%.

- Withholding tax on royalties: 10%.

- Business profits: Taxable in the source country only if a permanent establishment exists.

| Feature | US-Canada Tax Treaty | UK-Canada Tax Treaty | China-Canada Tax Treaty | India-Canada Tax Treaty |

| Dividends Withholding | 15% (5% for 10%+ corp) | 15% (5% for 10%+ corp) | 10% | 15% |

| Interest Withholding | Generally 0% | 0% | 10% | 15% |

| Royalties Withholding | 0% | 0% | 10% | 10% |

| Tax on Business Profits | Only with PE | Only with PE | Only with PE | Only with PE |

*PE: Permanent Establishment

How to Report Foreign Business Income in Canada?

Many foreign business owners panic thinking about handling foreign business income at first. The truth is, it may seem complex, but breaking it down into easier steps can make the process much smoother. Whether you’re a self-employed individual, a freelancer, or a business owner with income from abroad, it’s important to ensure that you report your foreign earnings accordingly. Keep reading this detailed guide on how to report your foreign business income in Canada, and you’ll be able to know all the reporting requirements to comply with Canadian tax laws.

Step 1: Gather Relevant Documents

Before knowing how to report foreign business income in Canada, you must collect all the necessary documents that support your earnings and expenses, such as:

- Income Statements: Documents from your foreign clients or business partners that indicate the income you have received.

- Invoices and Receipts: Evidence of your work or services provided, including any payments paid to you.

- Bank Statements: These statements are issued to confirm the exact amount of foreign income you have received.

- Tax Returns from the Foreign Country: In order to be eligible for a Foreign Tax Credit, you must include documents of taxes on the income you’ve earned in the country where your business is located.

Step 2: Complete the Required Form (Form T1135)

To know how to report foreign business income in Canada, you must first understand what appropriate tax forms to file. These forms ensure compliance with the Canada Revenue Agency (CRA). They help document your income, expenses, and foreign assets and claim applicable credits. Based on the nature of your work in foreign markets, you must file Form T1135.

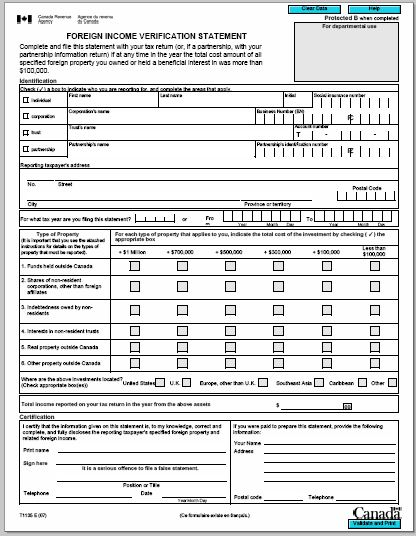

What is Form T1135?

The Form T1135, called Foreign Income Verification Statement, is solely to share your global income. Before knowing how to report foreign business income in Canada, you might wonder whether you must complete this form. Since Canada has a relationship with other nations, it is mandatory to file the proper forms to avoid tax evasion and the consequences of it.

Who must file Form T1135?

Any Canadian resident or corporation owning specified foreign property that costs more than $100,000 must file Form T1135. On top of that, certain partnerships with a specified foreign property that costs more than $100,000 are also obliged to file Form T1135.

Note: The cost of your SFP (specified foreign property) is the sum of the first payment and additional expenses (brokerage, legal fees, etc.). So, if you have purchased shares of a United States company for $30,000, your SFP costs $30,000 plus a $500 brokerage fee, making it a $30,500 asset.

What’s considered to be Specified Foreign Property?

The CRA has a long list of properties considered as specified foreign property. But generally speaking, SFP includes:

| Category | Description |

| Tangible and Intangible Assets | Buildings, land, or copyrights owned outside Canada by Canadian residents. |

| Convertible Properties | Assets that are convertible into or that provide benefits of acquiring foreign property. |

| Shares in Foreign Corporations | Stocks or shares of corporations established outside Canada. |

| Foreign Shares of Canadian Corporations | Shares of Canadian corporations operating abroad. |

| Loans to Non-Residents | Money lent to individuals or entities residing outside Canada. |

| Partnership Interests | Ownership in partnerships holding specified foreign property. |

| Precious Metals and Contracts | Precious metals, gold certificates, and futures contracts held abroad. |

| Mutual Fund Investments | Units of Canadian mutual funds that invest in foreign securities. |

| Foreign Business Property | Properties owned abroad for operating active businesses. |

| Foreign Insurance Policies | Interests in insurance policies issued outside Canada. |

What documents do you need to fill out Form T1135?

After listing your assets as SFP and non-SFP and calculating the exact cost, you must report them in Form T1135. You will need basic personal information like your Social Insurance Number to file this Form. You must also put some information about each SFP, including:

- Foreign Assets: Include detailed information about all specified foreign assets with the cost in the tax year.

- Asset Location: Specify the country code of the foreign company’s location.

- Asset Value and Costs: Record the highest value of each asset during the tax year and the original cost of each asset.

- Income Details: Report any income earned or losses from these foreign properties.

- Disposals and Gains/Losses: If you sold any assets during the tax year, include details of the sale along with any capital gains or losses.

What are the deadlines for filing Form T1135?

When you want to know how to report foreign business income in Canada, you must first meet the deadlines for filing Form T1135. It aligns with the due date of your income tax return and is different based on the business type.

| Business Type | Category | Deadline |

| Individuals | General | April 30 for the following tax year. |

| Self-Employed | June 15 if you, your spouse, or your common-law partner are self-employed. | |

| Corporation | General | Within the first six months after the corporation’s fiscal year ends. |

| Trusts | Inter Vivos Trusts | File within 90 days after December 31 (end of the tax year). |

| Testamentary Trusts | If the deceased passed between January 1 and October 31: File by April 30 of the same year. If the deceased passed between November 1 and December 31: File within six months of the date of death. | |

| Partnerships | Individual Partners | No later than March 31, after the partnership’s fiscal period ends. |

| Corporations | No later than five months after the partnership’s fiscal year ends. |

What are the penalties for errors in Form T1135?

If you are late to file Form T1135 on time, you will face a minimum of $100 and $25 for every day that you are late. The maximum penalty you may be subject to is $2,500. So, if you are late for 3 days, you must pay $100. But if you’re late for 15 days, you will have to pay ($25✖️15= $375)

Be careful to put only reliable and valid information in your Form. If you fail to do so and put inaccurate or incomplete information, you may be obligated to pay 50% of the understated tax as a penalty.

Failing to put valid information about your foreign income in Form T1135 might result in a three-year extension of the reassessment period, and the CRA will have access to review everything, not just the foreign business income.

How to report foreign business income in Form T1135?

Generally speaking, you have two methods of reporting: the simplified reporting method and the detailed reporting method. Before learning how to report foreign business income in Canada, you must first know which method of reporting is proper for you. The method you choose depends on the total cost amount for each asset during the tax year.

- Method A (Simplified Reporting Method)

This method is appropriate for those who own specified foreign property with more than CAD$100,000 total cost at any time of the year. However, it should be less than CAD$250,000 during the year. You only need to:

- Check the boxes for your property type.

- Choose the top three country codes where you hold most of your specified foreign property.

- Include the foreign business’ received income, gains, and losses.

- Method B (Detailed Reporting Method)

This method is appropriate for those who own specified foreign property with a total cost of CAD$250,000 or more at any time of the year. This part of Form T1135 has more complications.

The type of complicated information you should report in this part of Form T1135 includes:

- Name or description of the foreign entity.

- The country code of the country in which the foreign entity is located.

- Maximum cost amount during the year for each property and at the end of the year.

- The specified foreign property’s income, gains, or losses during the year.

Case Study: Reporting Foreign Business Income on Form T1135

Background: Don Malcovich, a Canadian resident, owns several foreign properties. Throughout the year, his foreign assets fluctuate in value and income generated. In 2024, John owned the following specified foreign properties:

- A rental property in the United States valued at CAD$150,000 at the start of the year.

- Shares in a European company were worth CAD$120,000 at the beginning of the year, which increased to CAD$180,000 by year-end.

- A bank account in Switzerland with CAD$50,000 deposited.

Applying the Reporting Methods

Method A: Simplified Reporting Method

Scenario: Don’s total foreign property at the beginning of the year is CAD$320,000, but it never exceeds CAD$250,000 at any time during the year. Therefore, he qualifies for the Simplified Reporting Method.

Steps for Reporting:

- Check Property Types:

- Real estate (rental property).

- Shares in foreign companies.

- Bank accounts.

- Top Three Country Codes:

- US (Rental Property)

- EU (Shares)

- CH (Bank Account in Switzerland)

- Report Income, Gains, and Losses:

- Rental Income: CAD$12,000 from the US property.

- Dividends: CAD$5,000 from the European company shares.

- Interest Income: CAD$1,500 from the Swiss bank account.

Method B: Detailed Reporting Method

Scenario: Suppose the value of Don’s shares in the European company surged to CAD$260,000 during the year, pushing the total cost of his foreign properties above CAD$250,000. In this case, he must use the Detailed Reporting Method.

Steps for Reporting:

- Name/Description of Foreign Entity:

- US Rental Property.

- European Company Shares.

- Swiss Bank Account.

- Country Codes:

- US (United States)

- EU (European Union)

- CH (Switzerland)

- Maximum Cost Amount During the Year:

- US Rental Property: CAD$150,000.

- European Company Shares: CAD$260,000.

- Swiss Bank Account: CAD$50,000.

- Year-End Cost Amount:

- US Rental Property: CAD$150,000.

- European Company Shares: CAD$180,000.

- Swiss Bank Account: CAD$50,000.

- Income, Gains, or Losses:

- Rental Income: CAD$12,000 (US).

- Dividends: CAD$5,000 (EU).

- Interest Income: CAD$1,500 (CH).

Step 3: Calculating and Claiming the Foreign Tax Credit

If you’re a Canadian citizen earning income from a business outside Canada’s borders, you can avoid being taxed twice by claiming a foreign tax credit. This credit can help you reduce your Canadian taxes by the amount of tax you’ve already paid in the country where your business is located.

To be eligible to receive the foreign tax credit, you must have been a citizen of Canada on December 31 of the current tax year or the last day of your residence in Canada. Before knowing how to report foreign business income in Canada, you must be aware of calculating the foreign tax credit.

You must complete Form T2209 (Federal Foreign Tax Credits) to receive the foreign tax credit. Once you have completed this form, you must attach the documents of foreign taxes paid or receipts from the foreign country along with the tax returns.

If you’re a Canadian earning income while working remotely for a US company and need a detailed guide on how to pay taxes, check out the article Canadian Working Remotely for US Company Taxes.

Step 4: Filing Your Tax Return

Once you make sure you’ve done all the previous steps, you may now submit your tax returns with the CRA. This is the most crucial step, as it ensures the CRA that you’ve attached accurate information and completely comply with Canadian tax rules.

Verify and double-check all the details in the gathered documents to ensure no errors, like:

- The exact amount of foreign business income with eligible deductions applied to it

- Form T2209 (Federal Foreign Tax Credits)

- Supporting documentation, such as receipts or foreign tax payment proof

- Form T1135 (Foreign Income Verification Statement)

Note: I urge you to check your CRA account regularly after submitting your tax returns to receive the confirmation that it has been processed.

Common Tax Challenges and Solutions

Incorporating a business outside of Canada is challenging enough. You don’t want to make it more complicated by not complying with Canadian tax regulations and face penalties. There are some key challenges that every Canadian foreign business owner might face when reporting foreign business income. But what are those challenges and how can you navigate these complexities while maximizing tax benefits?

Avoiding Double Taxation

After learning how to report foreign business income in Canada, a major concern for Canadian business owners is the fear of being taxed twice. To address this, I leverage foreign tax credits for the taxes they already paid in the other country. This ensures that my clients only pay any excess tax owed in Canada.

Determining Permanent Establishment

Many business owners in Canada mistakenly report income in foreign countries where they didn’t have to. Especially for businesses in the US, the US-Canada Tax Treaty points out some key considerations regarding whether a company has a permanent establishment (PE) in a foreign country:

- Employees, Offices, or Warehouses: Having employees, office spaces, or warehouses in a foreign country often establishes a PE.

- Third-Party Logistics (3PL): Using 3PL providers for storage is acceptable, but owning a dedicated storage space typically establishes a PE.

- Agents with Binding Authority: Agents who can sign agreements on behalf of the business are considered part of a PE, while independent sales agents without such authority are not.

- Service-Based and E-Commerce Businesses: Many service companies and drop-shipping brands often lack these indicators and, as a result, do not need to report income in the foreign country.

Filing Required Canadian Tax Forms

While the steps to know how to report foreign business income in Canada are easy and straightforward, sometimes Canadian foreign business owners fail to file the appropriate tax forms.

Form T1134: This is a form that indicates whether the Canadian taxpayers own a business in the foreign countries or have significant interests in foreign affiliates.

The form must be filed within 10 months of the taxpayer’s year-end.

Failure to file T1134 on time can result in a penalty of $25 per day (minimum $100) for up to 100 days of non-compliance.

For clients who don’t have enough financial data from their foreign business, I simplify the process by ticking the box that indicates there is not enough financial data. This adjustment reduces the complexity of the form.

Final Words

In this article, I covered everything you must know about how to report foreign business income in Canada. I walked you through the small details and complications of reporting foreign business income. However, you might still find it challenging to do the whole process yourself. That is why our team at SAL Accounting is ready to help you with whatever minor or significant inconvenience you might face along the way! Book a FREE consultation with our CPA and ensure you’re on the right track.

FAQ

To report foreign employment income in Canada that you earned during the year that wasn’t included on a T4, search for “Foreign Employment” in the search bar, then include the “Other Foreign Income & Foreign Tax Credits” section in your tax return.

Any foreign business income that is related to these three categories can’t receive the tax credit:

- The foreign business income that is tax-free in Quebec or Canada under a particular tax rule.

- The foreign business income that is free of tax from foreign income tax.

- Foreign business income allocated to a beneficiary, such as through a trust.

Foreign business income in Canada is the income or loss you receive from owning property, shares, interests in partnerships, mutual trust funds, etc., somewhere outside Canada. You can receive a tax credit for your foreign business income to avoid double taxation.

Yes, even if you have already paid taxes in another country, you must report your foreign business income in Canada. You can claim the tax as a foreign tax, which will reduce the tax the CRA expects you to pay.

The form you must file as a Canadian with foreign business income is Form T1135, Foreign Income Verification Statement. Canadian residents or corporations that own a specified foreign property that costs more than $100,000 at any time of the year are obliged to file this Form.

If you realize you’ve made a mistake while reporting foreign business income, immediately file an adjustment request using the CRA’s My Account or mail Form T1-ADJ to correct your tax return. Prompt corrections can help avoid penalties.

If your total foreign business income is less than CAD 100,000, you don’t need to file Form T1135, as Form T1135 is only for business owners with more than CAD 100,000 incomes. However, you must still report your foreign business income on your T1 General tax return.

In order to know how to report foreign business income in Canada, you must convert the foreign income you’ve earned to Canadian dollars. You must use the exchange rate on the date you have earned it. Given the minimal fluctuations, you may also use the annual average exchange rate. The CRA approves the exchange rate from some sources, like the Bank of Canada and CRA-approved services.

Yes, Form T1135 can be filed online. Individuals can use the CRA’s My Account portal or certified tax software to submit the form electronically. Corporations and trusts can file through their account on the CRA website or use authorized software. Tax professionals can also submit the form using the Represent a Client service. Filing the form online is much more efficient than filing a paper form. It’s best to submit your form online to save time. Before filing Form T1135, check all required details, such as property descriptions, country codes, and income amounts, before submission.